An Introduction to Statistical Programming Methods with R

Once you have learned RMarkdown and GitHub, feel free to make a pull request to offer bug fixes or corrections!

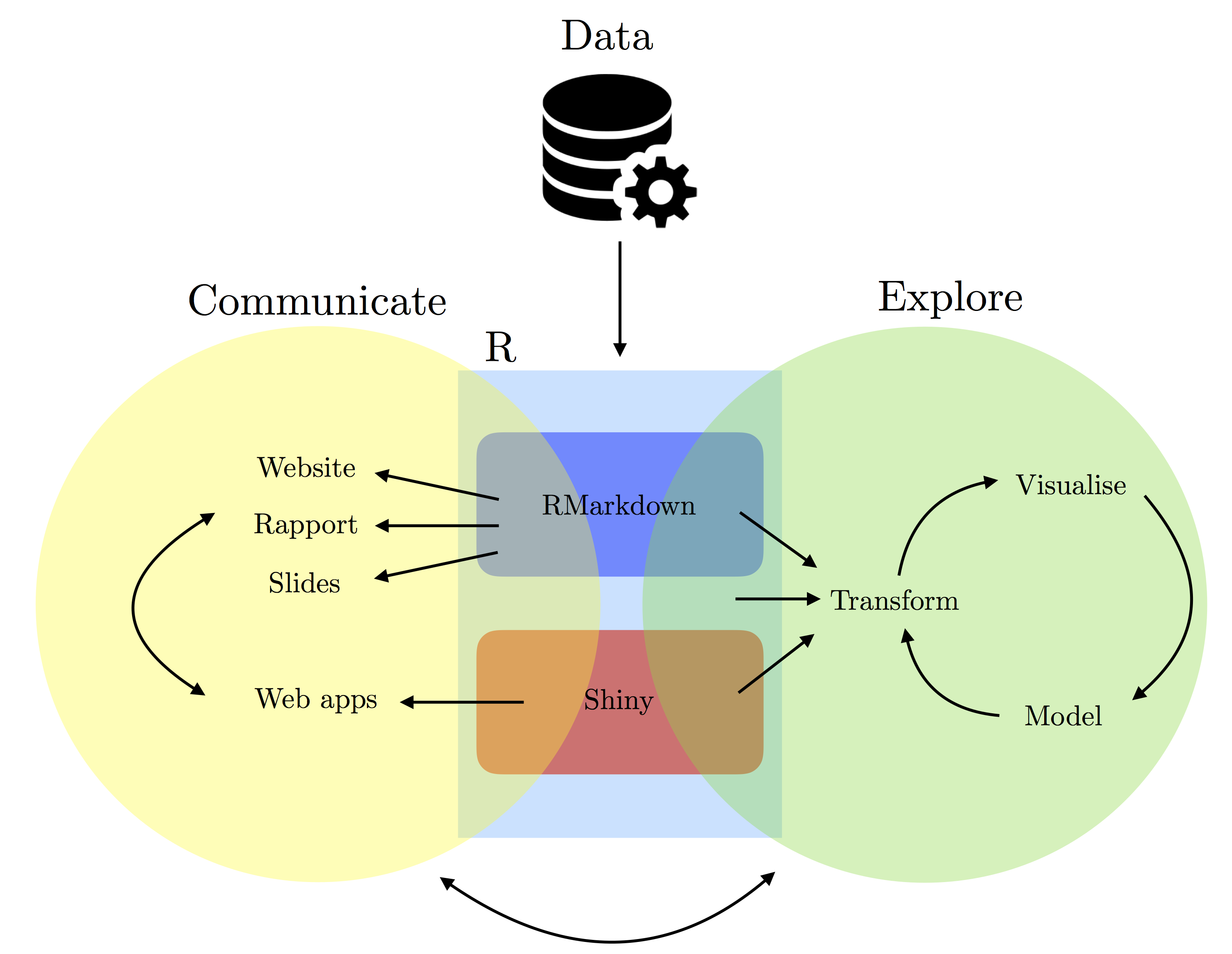

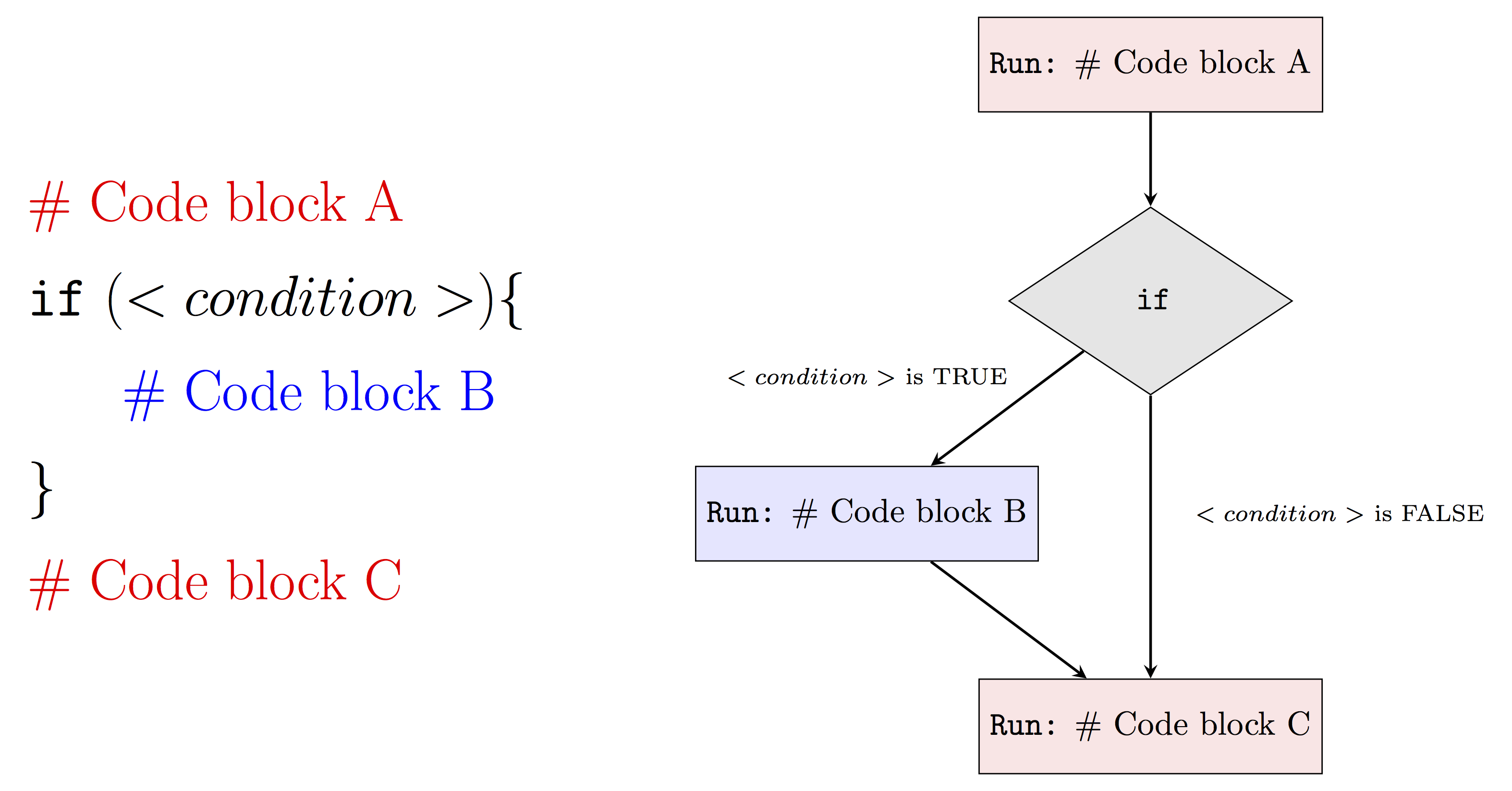

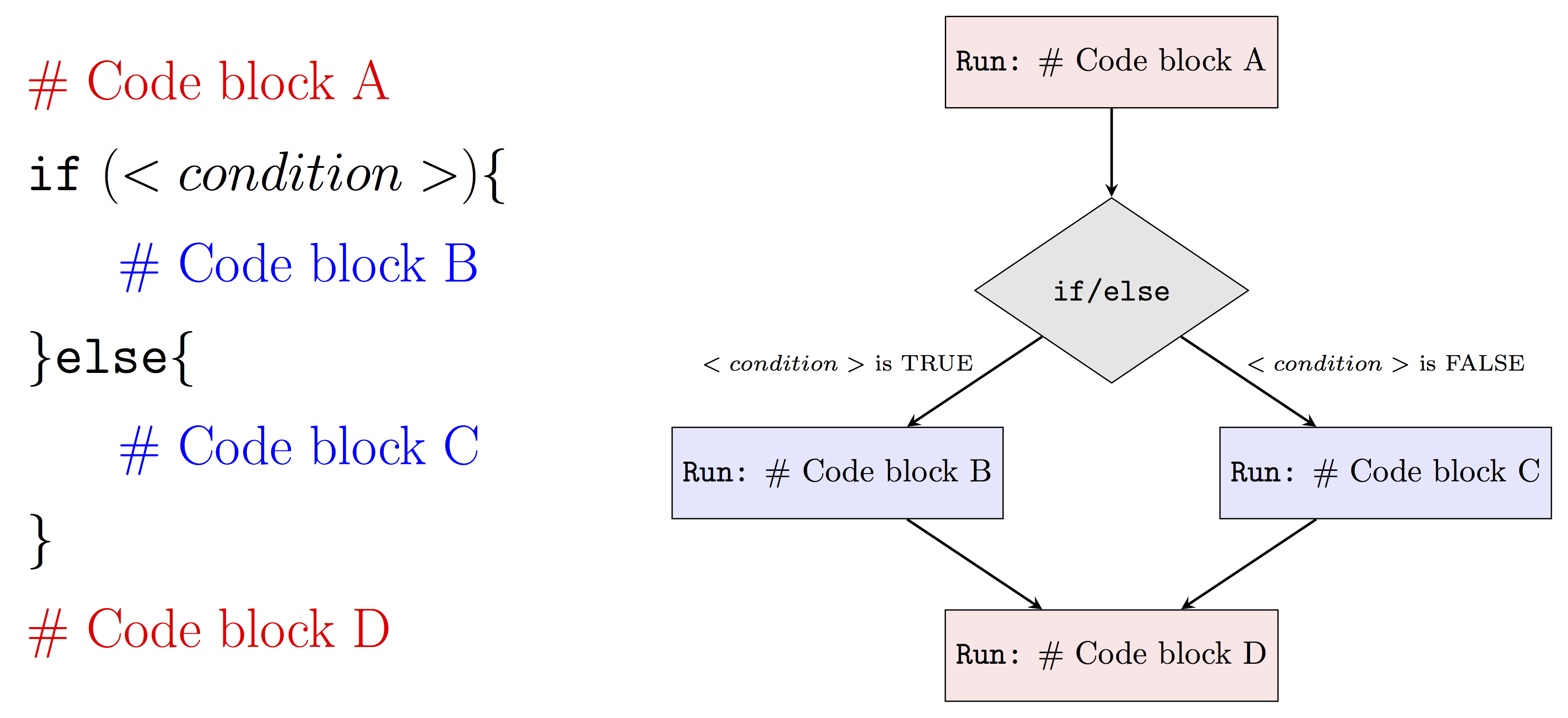

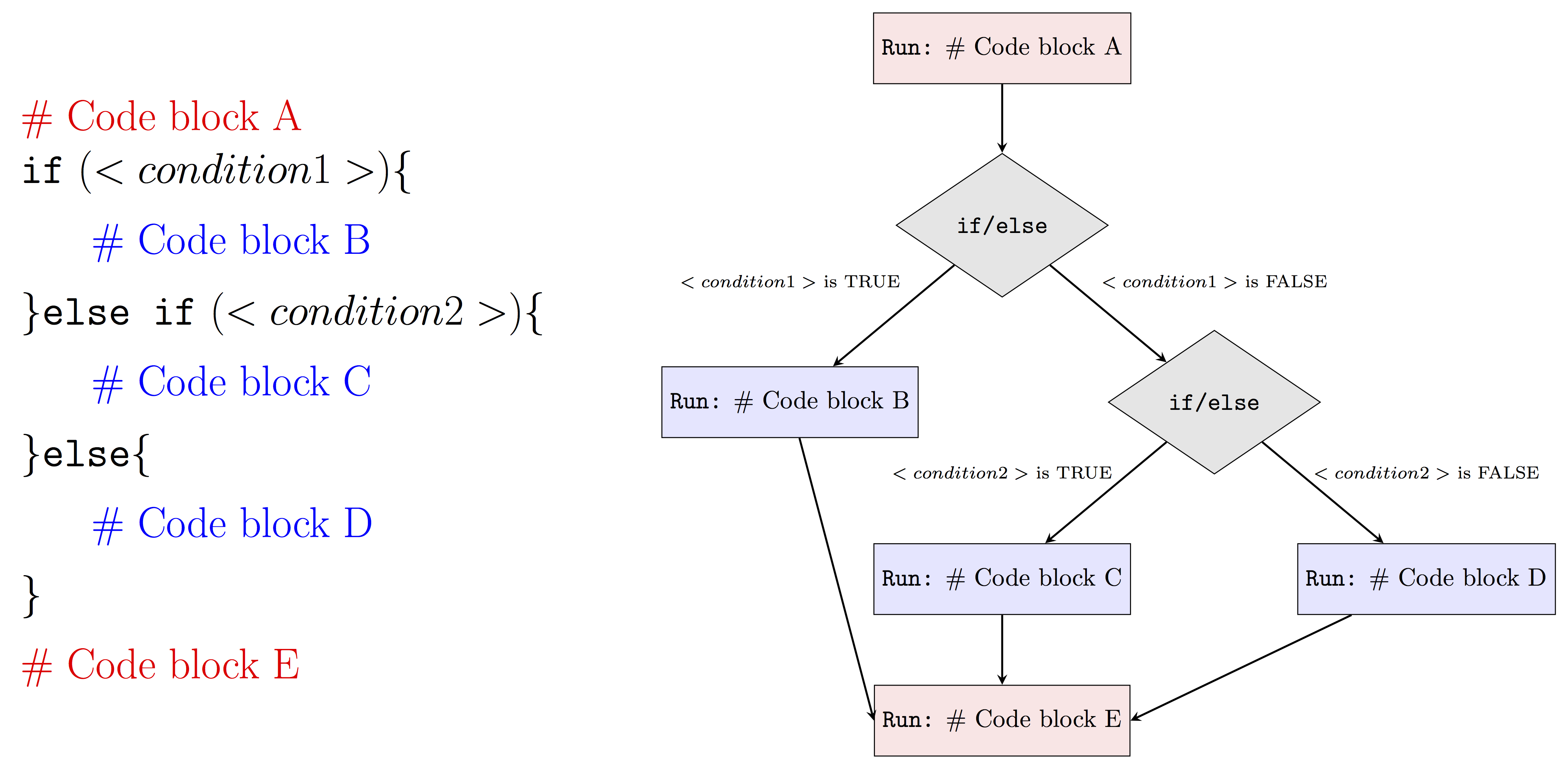

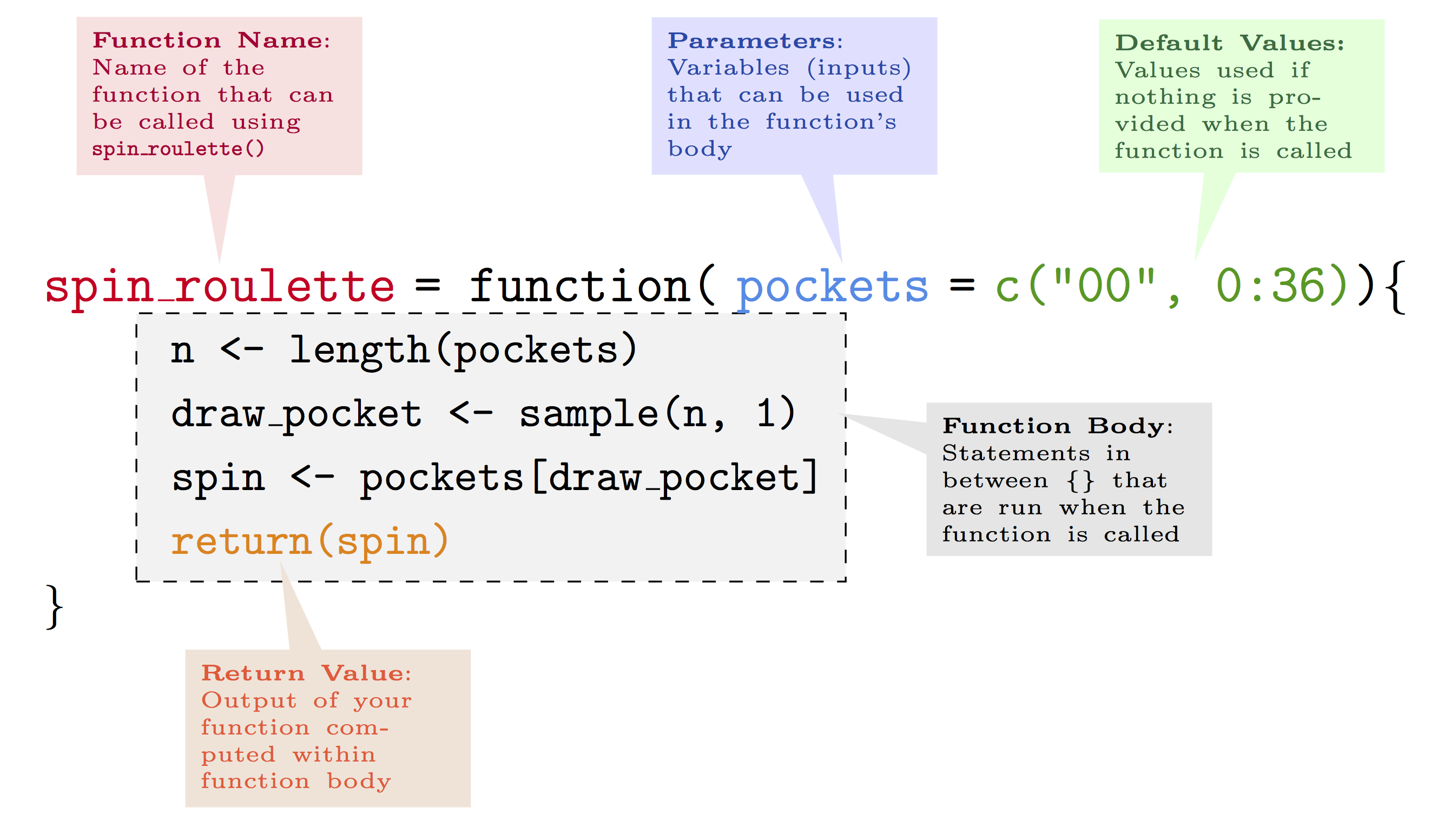

To highlight our goals, we will roughly follow the process that is represented in the diagram above.

Indeed, in many cases, an input (e.g. data source) is provided, and then we process, explore, and/or manipulate the data with R.

Once this is done, we then can communicate our findings through websites, reports, slides, etc.

using some combination of RMarkdown, R and/or Shiny.

This process is not always sequential since we can often have new ideas or observations at any stage this process therefore bringing us back to exploring the data again.

1.1 R and RStudio

1.1.1 Getting started with R

Since R is a free and open-source software, you may simply download it from the following link:

R: https://cran.r-project.org/

While R certainly can be used "as is" for many purposes, we strongly recommend using an IDE called RStudio.

There are several versions of RStudio for different users (RStudio Desktop, Commercial, Server, etc.).

The free RStudio Desktop version is sufficient for our purposes.

RStudio can downloaded from the following link:

RStudio: https://www.rstudio.com/

You cannot use RStudio without having installed R on your computer.

1.1.2 Why R?

There are many reasons to use R.

Two compelling reasons are that R is both free as in "free pizza", and free as in "free speech".

The fact that is a free and open-source software does not necessarily imply that it is a good software (although it is also that).

1.1.3 About RStudio

Below is short video demonstrating a basic introduction of RStudio and some of its elements.

In addition, RStudio provides embedded functionality to utilize collaborative version-control software including GitHub & Subversion as well as a set of powerful tools to save and communicate results (whether they be simulations, data analysis, or presenting and making available a new package to other users).

Some examples of these tools are Rmarkdown which can be used respectively to integrate written narrative with embedded R code and other content, as well as and Shiny Web Apps which can provide an interactive user-friendly interface that permits a user to actively engage with a wide variety of tools built in R without the need to encounter raw R code.

GitHub and Rmarkdown will be the object of a more in-depth description in the first chapters of this book in order to provide the reader with the version-control and annotation tools that can be useful for the following chapters of this book.

1.1.4 Conventions

Throughout this book, R code will be typeset using a monospace font which is syntax highlighted.

For example:

a = pi

b = 0.5

sin(a*b)

Similarly, R output lines (that usally appear in your Console) will begin with ## and will not be syntax highlighted.

The output of the above example is the following:

## [1] 1

Aside from R code and output, this book will also insert boxes in order to draw the reader’s attention to important, curious, or otherwise informative details.

Therefore the following boxes and symbols can be used to represent information of different nature:

1.1.5 Getting help

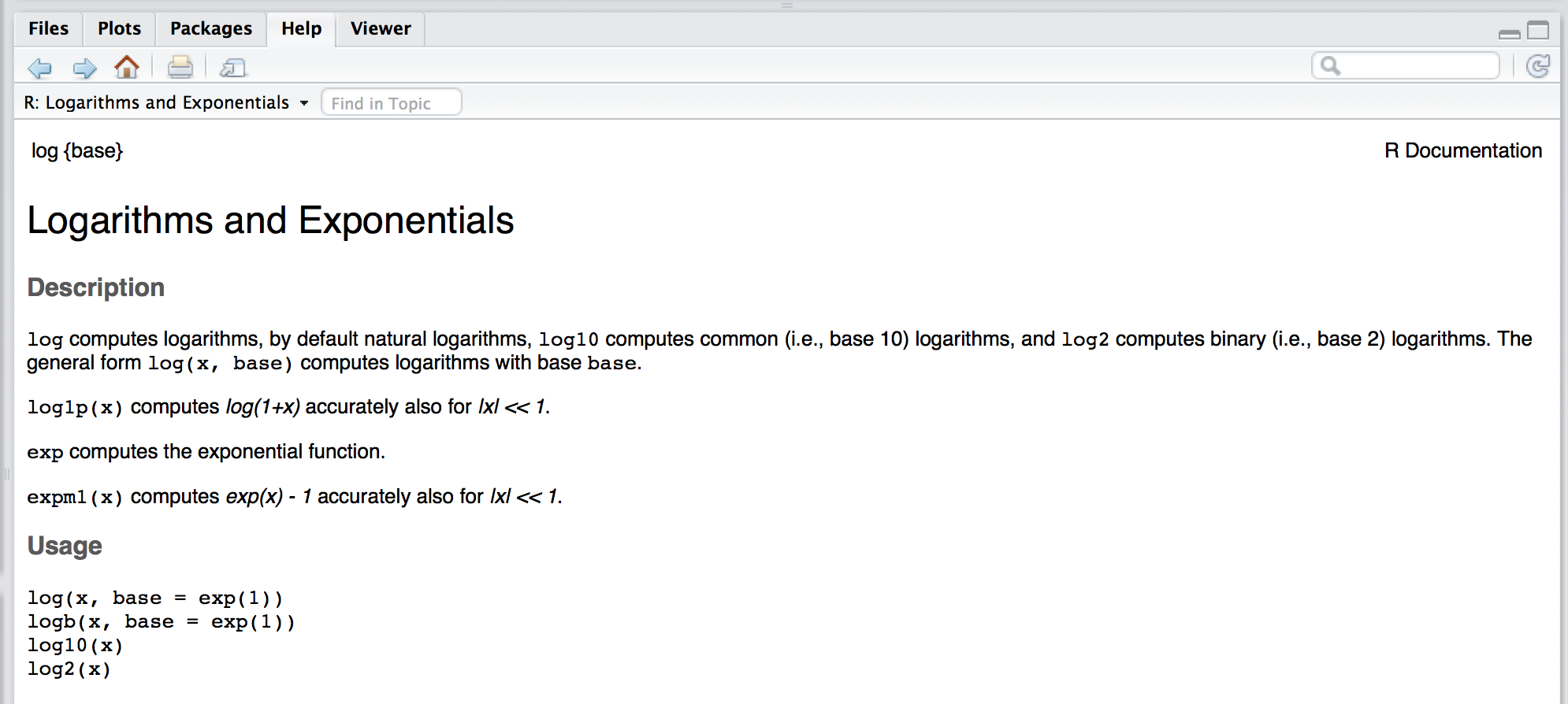

In the previous section we presented some examples on how R can be used as a calculator and we have already seen several functions such as sqrt() or log().

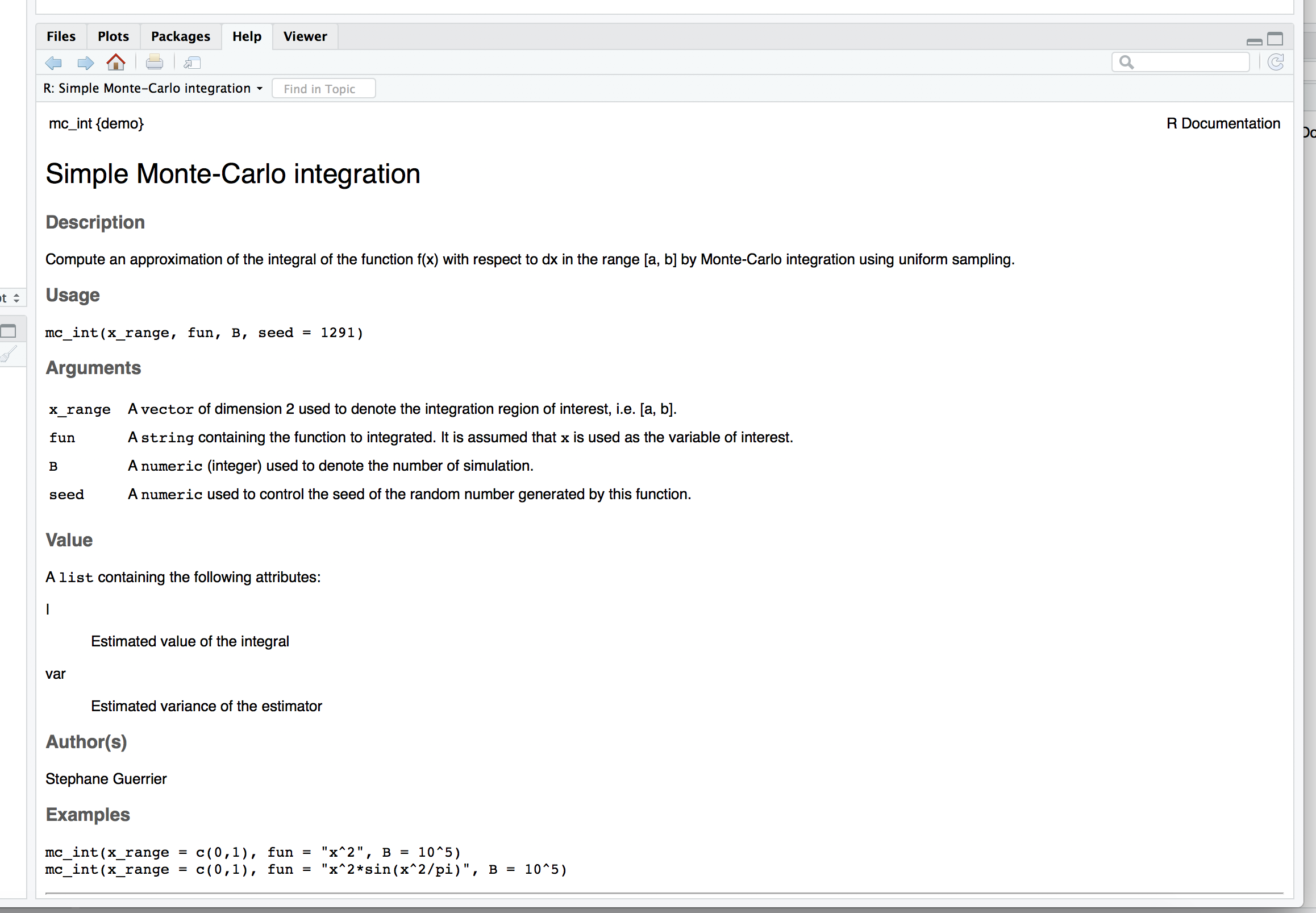

To obtain documentation about a function in R, simply put a question mark in front of the function name (or just type help() around the function name), or use the search bar on the "Help" tab in your RStudio window, and its documentation will be displayed.

For example, if you are interested in learning about the function log() you could simply type:

?log

which will display something similar to:

The R documentation is written by the author of the package.

For mainstream packages in widespread use, the documentation is almost always quite good, but in some cases it can be quite technical, difficult to interpret, and possibly incomplete.

In these cases, the best solution to understand a function is to search for help on any search engine.

Often a simple search like "side by side boxplots in R" or "side by side boxplots in ggplot2" will produce many useful results.

The search results often include user forums such as "CrossValidated" or "StackExchange" in which the questions you have about a function have probably already been asked and answered by many other users.

You can often use the error message to search for answers about a problem you may have with a function.

1.1.6 Installing packages

R comes with a number of built-in functions but one of its main strengths is that there is a large number of packages on an ever-increasing range of subjects available for you to install.

These packages provide additional functions, features and data to the R environement.

If you want to do something in R that is not available by default, there is a good chance that there are packages that will respond to your needs.

In this case, an appropriate way to find a package in R is to use the search option in the CRAN repository which is the official network of file-transfer protocols and web-servers that store updated versions of code and documentation for R (see CRAN website).

Another general approach to find a package in R is simply to use a search engine in which to type the keywords of the tools you are looking for followed by "R package".

R packages can be installed in various ways but the most widely used approach is through the install.packages() function.

Another way is to use the "Tools -> Install Packages…" path from the dropdown menus in RStudio or clicking on the "install" button in the "Packages" pane in the RStudio environment.

The install.packages() function is very straight-forward and transcends any platform for the R environment.

It is noteworthy that this approach assumes that the desired package(s) are available within the CRAN repository.

This is very often the case, but there is a growing number of packages that are under-development or completed and are made available through other repositories.

In the latter setting, Chapter 02 will show other ways of installing packages from a commonly used repository called "GitHub".

Sticking momentarily to the packages available in the CRAN repository, the use of the install.packages() is quite simple.

For example, if you want to install the package devtools you can simply write:

install.packages("devtools")

Once a package is installed it is not directly usable within your R session.

To do so you will have to "load" the package into your current R session which is generally done through the function library().

For example, after having installed the devtools package, in order to use it within your session you would write:

library(devtools)

Once this is done, all the functions and documentation of this package are available and can be used within your current session.

However, once you close your R session, all loaded packages will be closed and you will have to load them again if you want to use them in a new R session.

Please notice that although packages need to be loaded at each session if you want to use them, they need to be installed only once.

The only exception to this rule is when you need to update the package or reinstall it for some reason.

One of the main packages that is required for this class would be our introDS package, that contains all the necessary packages and functions that will be utilized in this book.

Run the following code to install the package directly from GitHub.

install_github("SMAC-Group/introDS")

The introDS package is required for use of many features in this book.

1.1.7 Additional References

There are many more elements in RStudio, and we encourage you to use the RStudio Cheatsheet as a reference.

1.2 Basic Probability and Statistics with R

The R environment provides an up-to-date and efficient programming language to develop different tools and applications.

Nevertheless, its main functionality lies in the core statistical framework and tools that consistute the basis of this language.

Indeed, this book aims at introducing and describing the methods and approaches of statistical programming which therefore require a basic knowledge of Probability and Statistics in order to grasp the logic and usefulness of the features presented in this book.

For this reason, we will briefly take the reader through some of the basic functions that are available within R to obtain probabilities based on parametric distributions, compute summary statistics and understand basic data structures.

The latter is just an introduction and a more in-depth description of different data structures will be given in a future chapter.

1.2.1 Simple calculations

Since the R environment can serve as an advanced calculator, it is worth noting this also allows for simple calculations.

In the table below we show a few examples of such calculations where the first column gives a mathematical expression (calculation), the second gives the equivalent of this expression in R and finally in the third column we can find the result that is output from R.

Math.

R

Result

2+2

2+2

4

(frac{4}{2})

4/2

2

(3 \cdot 2^{-0.8})

3*2^(-0.8)

1.723048

(sqrt{2})

sqrt(2)

1.414214

(pi)

pi

3.141593

(ln(2))

log(2)

0.6931472

(log_{3}(9))

log(9, base = 3)

2

(e^{1.1})

exp(1.1)

3.004166

(cos(sqrt{0.9}))

cos(sqrt(0.9))

0.5827536

1.2.2 Probability Distributions

Probability distributions can be uniquely characterized by different functions such as, for example, their density or distribution functions.

Based on these it is possible to compute theoretical quantiles and also randomly sample observations from them.

Replacing the R syntax for a given probability distribution with the general syntax name, all these functions and calculations are made available in R through the built-in functions:

dname calculates the value of the density function (pdf);

pname calculates the value of the distribution function (cdf);

qname calculates the value of the theoretical quantile;

rname generates a random sample from a particular distribution.

Note that, when using these functions in practice, name is replaced with the syntax used in R to denote a specific probability distribution.

For example, if we wish to deal with a Uniform probability distribution, then the syntax name is replaced by unif and, furthering the example, to randomly generate observations from a uniform distribution the function to use will be therefore runif.

R allows to make use of these functions for a wide variety of probability distributions that include, but are not limited to: Gaussian (or Normal), Binomial, Chi-square, Exponential, F-distribution, Geometric, Poisson, Student-t and Uniform.

In order to get an idea of how these functions can be used, below is an example of a problem that can be solved using them.

1.2.2.1 Example: Normal Test Scores of College Entrance Exam

Assume that the test scores of a college entrance exam follows a Normal distribution.

Furthermore, suppose that the mean test score is 70 and that the standard deviation is 15.

How would we find the percentage of students scoring 90 or more in this exam?

In this case, we consider a random variable (X) that is normally distributed as follows: (X sim N(mu=70, \sigma^2=225)) where (mu) and (sigma^2) represent the mean and variance of the distribution respectively.

Since we are looking for the probability of students scoring higher than 90, we are interested in finding (mathbb{P}(X > x=90)) and therefore we look at the upper tail of the Normal distribution.

To find this probability we need the distribution function (pname) for which we therefore replace name with the R syntax for the Normal distribution: norm.

The distribution function in R has various parameters to be specified in order to compute a probability which, at least for the Normal distribution, can be found by typing ?pnorm in the Console and are:

q: the quantile we are interested in (e.g. 90);

mean: the mean of the distribution (e.g. 70);

sd: the standard deviation of the distribution (e.g. 15);

lower.tail: a boolean determining whether to compute the probability of being smaller than the given quantile (i.e. (mathbb{P}(X \leq x))) which requires the default argument TRUE or larger (i.e. (mathbb{P}(X > x))) which requires to specify the argument FALSE.

Knowing these arguments, it is now possible to compute the probability we are interested in as follows:

pnorm(q = 90, mean = 70, sd = 15, lower.tail = FALSE)

## [1] 0.09121122

As we can see from the output, there is roughly a 9% probability of students scoring 90 or more on the exam.

1.2.3 Summary Statistics

While the previous functions deal with theoretical distributions, it is also necessary to deal with real data from which we would like to extract information.

Supposing–as is often the case in applied statistics–we don’t know from which distribution it is generated, we would be interested in understanding the behavior of the data in order to eventually identify a distribution and estimate its parameters.

The use of certain functions varies according to the nature of the inputs since these can be, for example, numerical or factors.

1.2.3.1 Numerical Input

A first step in analysing numerical inputs is given by computing summary statistics of the data which, in this section, we can generally denote as x (we will discuss the structure of this data more in detail in the following chapters).

For central tendency or spread statistics of a numerical input, we can use the following R built-in functions:

mean calculates the mean of an input x;

median calculates the median of an input x;

var calculates the variance of an input x;

sd calculates the standard deviation of an input x;

IQR calculates the interquartile range of an input x;

min calculates the minimum value of an input x;

max calculates the maximum value of an input x;

range returns a vector containing the minimum and maximum of all given arguments;

summary returns a vector containing a mixture of the above functions (i.e. mean, median, first and third quartile, minimum, maximum).

1.2.3.2 Factor Input

If the data of interest is a factor with different categories or levels, then different summaries are more appropriate.

For example, for a factor input we can extract counts and percentages to summarize the variable by using table.

Using functions and data structures that will be described in the following chapters, below we create an example dataset with 90 observations of three different colors: 20 being Yellow, 10 being Green and 50 being Blue.

We then apply the table function to it:

table(as.factor(c(rep("Yellow", 20), rep("Green", 10), rep("Blue", 50))))

##

## Blue Green Yellow

## 50 10 20

By doing so we obtain a frequency (count) table of the colors.

1.2.3.3 Dataset Inputs

In many cases, when dealing with data we are actually dealing with datasets (see Chapter 03) where variables of different nature are aligned together (usually in columns).

For datasets there is another convenient way to get simple summary statistics which consists in applying the function summary to the dataset itself (instead of simply a numerical input as seen earlier).

As an example, let us explore the Iris flower dataset contained in the R built-in datasets package.

The data set consists of 50 samples from each of three species of Iris (Setosa, Virginica and Versicolor).

Four features were measured from each sample consisting in the length and the width (in centimeters) of the both sepals and petals.

This dataset is widely used as an example since it was used by Fisher to develop a linear discriminant model based on which he intended to distinguish the three species from each other using combinations of these four features.

Using this dataset, let us use the summary function on it to output the minimum, first quartile and thrid quartile, median, mean and maximum statistics (for the numerical variables in the dataset) and frequency counts (for factor inputs).

summary(iris)

## Sepal.Length Sepal.Width Petal.Length Petal.Width

## Min.

:4.300 Min.

:2.000 Min.

:1.000 Min.

:0.100

## 1st Qu.:5.100 1st Qu.:2.800 1st Qu.:1.600 1st Qu.:0.300

## Median :5.800 Median :3.000 Median :4.350 Median :1.300

## Mean :5.843 Mean :3.057 Mean :3.758 Mean :1.199

## 3rd Qu.:6.400 3rd Qu.:3.300 3rd Qu.:5.100 3rd Qu.:1.800

## Max.

:7.900 Max.

:4.400 Max.

:6.900 Max.

:2.500

## Species

## setosa :50

## versicolor:50

## virginica :50

##

##

##

1.3 Main References

This is not the first (or the last) book that has been written explaining and describing statistical programming in R.

Indeed, this can be seen as a book that brings together and reorganizes information and material from other sources structuring and tailoring it to a course in basic statistical programming.

The main references (which are far from being an exhaustive review of literature) that can be used to have a more in-depth view of different aspects treated in this book are:

Wickham (2014a) : a more technical and advanced introduction to R;

basic building blocks of building packages in R;

Xie (2015) : an overview of document generation in R;

1.4 License

You can redistribute it and/or modify this book under the terms of the Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License (CC BY-NC-SA) 4.0 License.

Chapter 2 RMarkdown

RMarkdown is a framework that provides a literate programming format for data science.

It can be used to save and execute R code within RStudio and also as a simple formatting syntax for authoring HTML, PDF, ODT, RTF, and MS Word documents as well as seamless transitions between available formats.

The name "markdown" is an intentional contrast to other "markup" languages–e.g., hypertext markup language (HTML)–which require syntax that can be quite difficult to decipher for the uninitiated.

One aim of the markdown paradigm is a syntax that is as human-readable as possible.

"RMarkdown" is an implementation of the "markdown" language designed to accommodate embedded R code.

What is literate programming ?

Literate programming is the notion for programmers of adding narrative context with code to produce documentation for the program simultaneously.

Consequently, it is possible to read through the code with explanations so that any viewer can follow through the presentation.

RMarkdown offers a simple tool that allows to create reports or presentation slides in a reproducible manner with collateral advantages such as avoiding repetitive tasks by, for example, changing all figures when data are updated.

What is reproducible research ?

Reproducible research or reproducible analysis is the notion that an experiment’s whole process, including collecting data, performing analysis and producing output, can be reproduced the same way by someone else.

Building non-reproducible experiments has been a problem both in research and in the industry, and having such an issue highly decreases the credibility of the authors’ findings and, potentially, the authors themselves.

In essence, allowing for reproducible research implies that anyone could run the code (knit the document, etc.) and obtain the same exact results as the original research and RMarkdown is commonly used to address this issue.

Below is a short video showing a basic overview of RMarkdown.

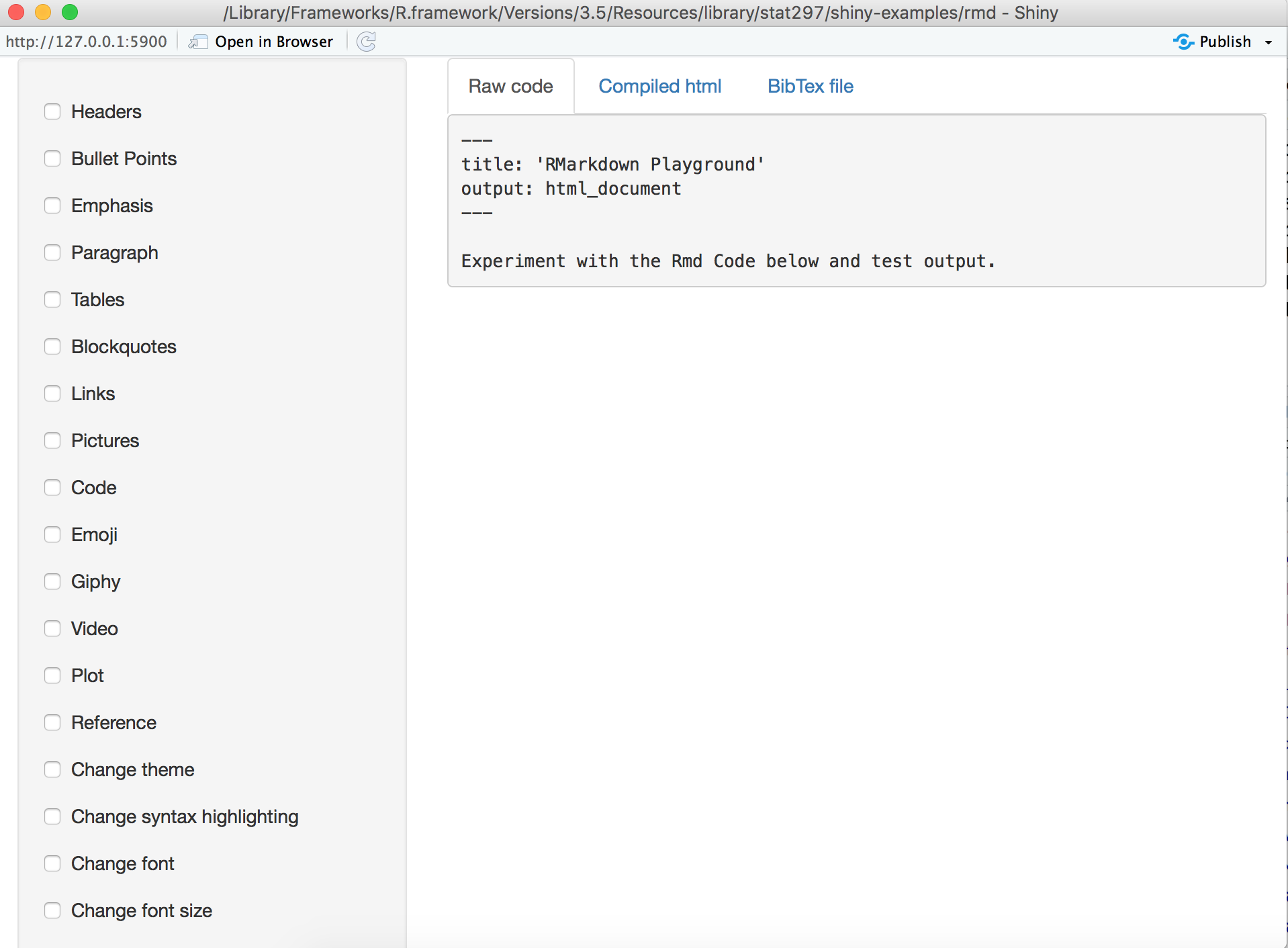

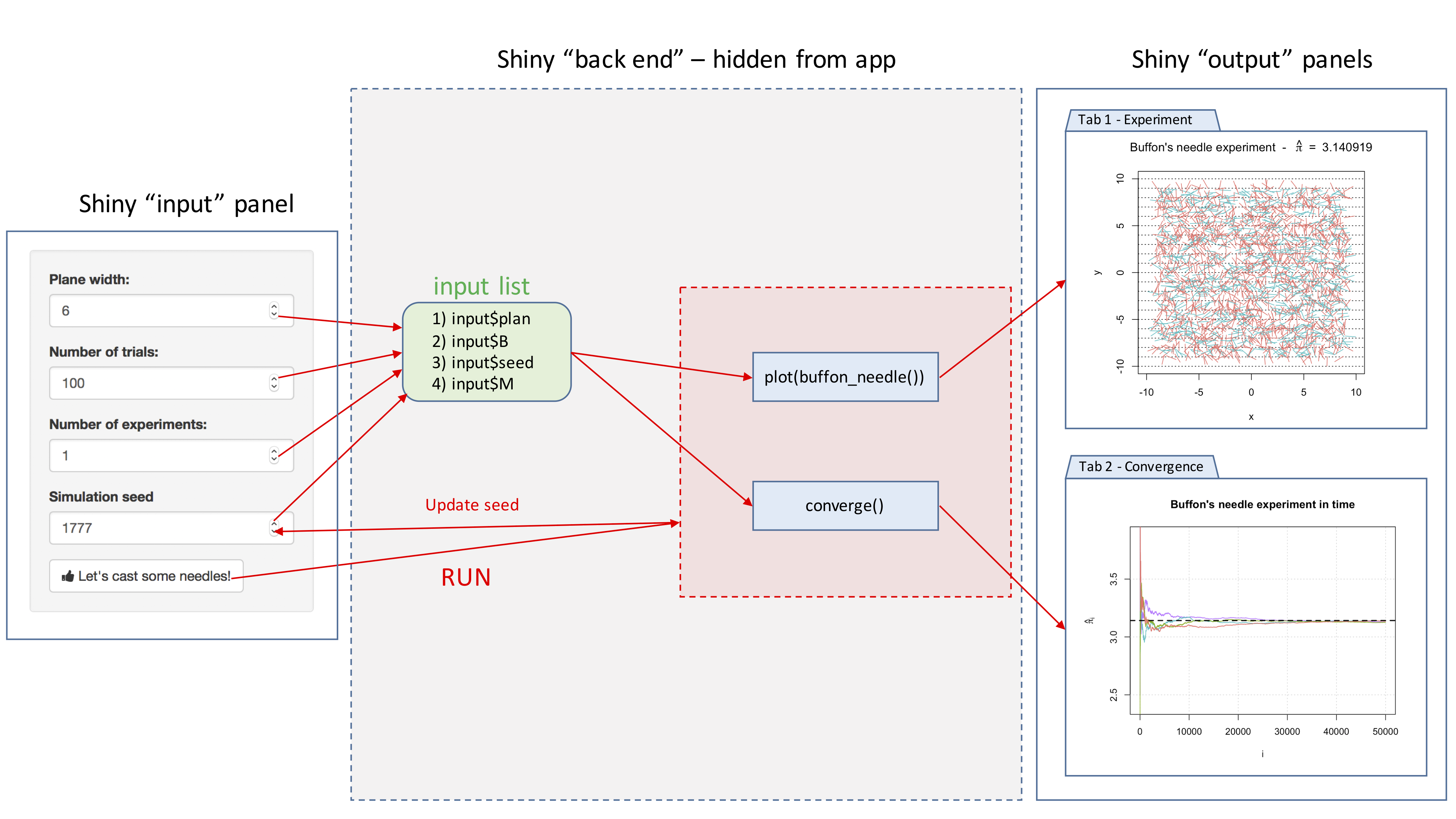

We have created a framework application that you can use to test out different RMarkdown functions.

Simply run the following code within the introDS package by using either

# RMarkdown Web

introDS::runShiny('rmd')

# RMarkdown Mobile

introDS::runShiny('rmd_mini')

Then a shiny app window will pop out for you to access the application like the following:

As you can see, the toolbar on the left hand side allows you to try different RMarkdown functions.

On the right hand side, Raw code shows the original R code that generates the output, Compiled html shows the compiled output based on the Raw code, and BibTex file shows the formatting lists of references.

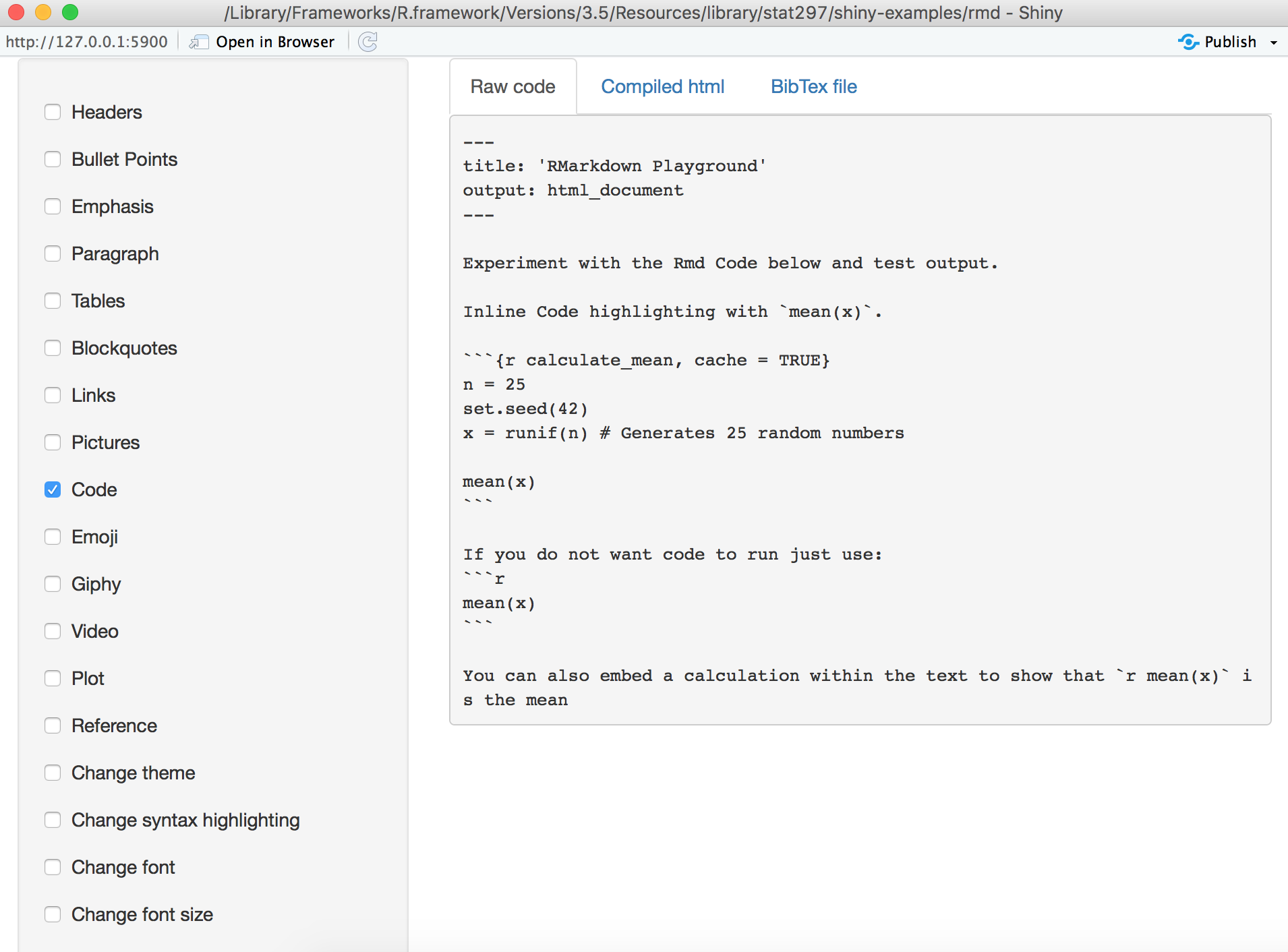

For example, let’s try to compile some R code within RMarkdown.

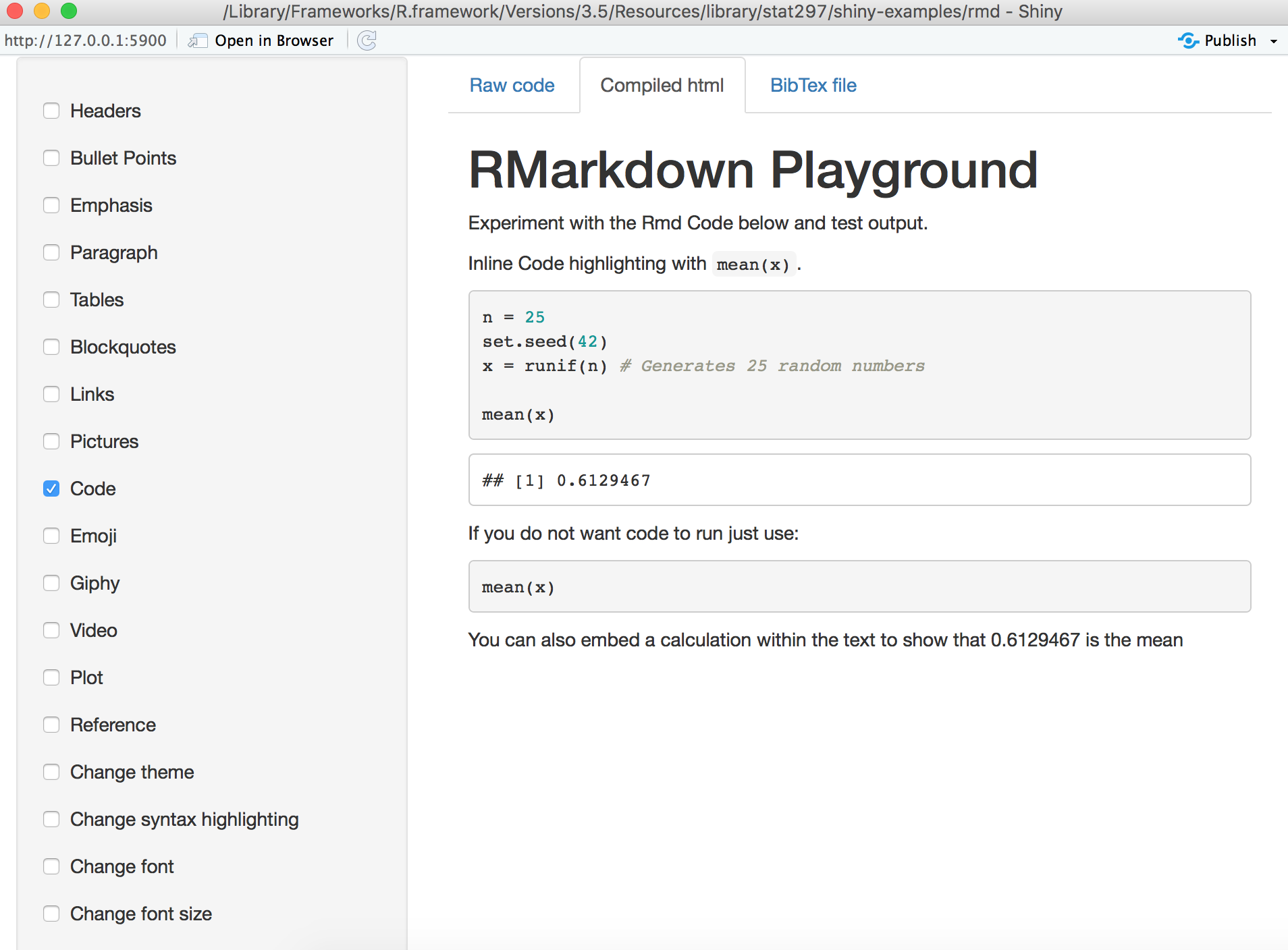

Click on the Code in the toolbar for some example code:

Then when we click on the Compiled html, we can see the following output:

You can also try multiple functions at the same time.

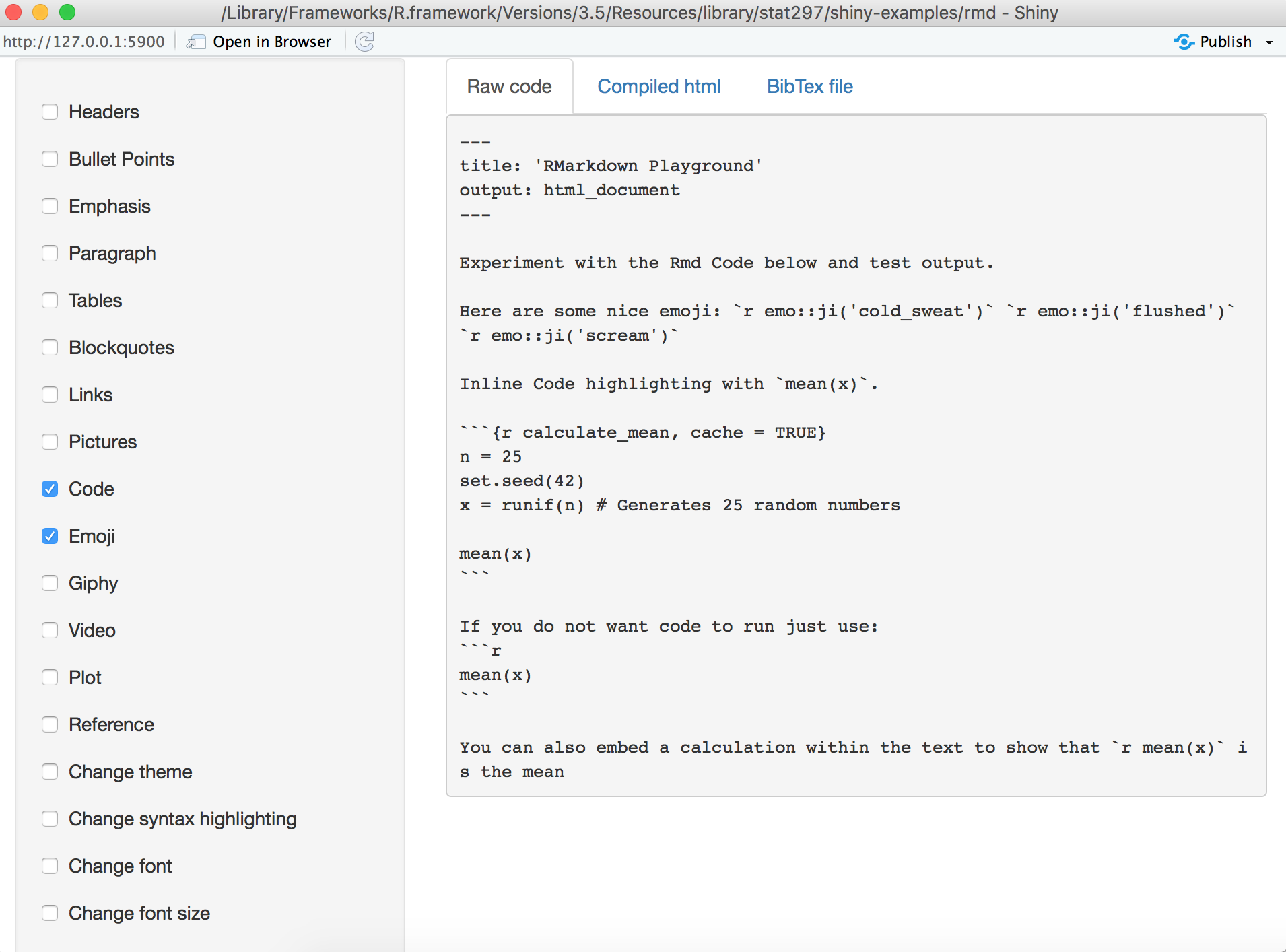

For example, let’s click both Code and Emoji in the toolbar, we can see the following R code used:

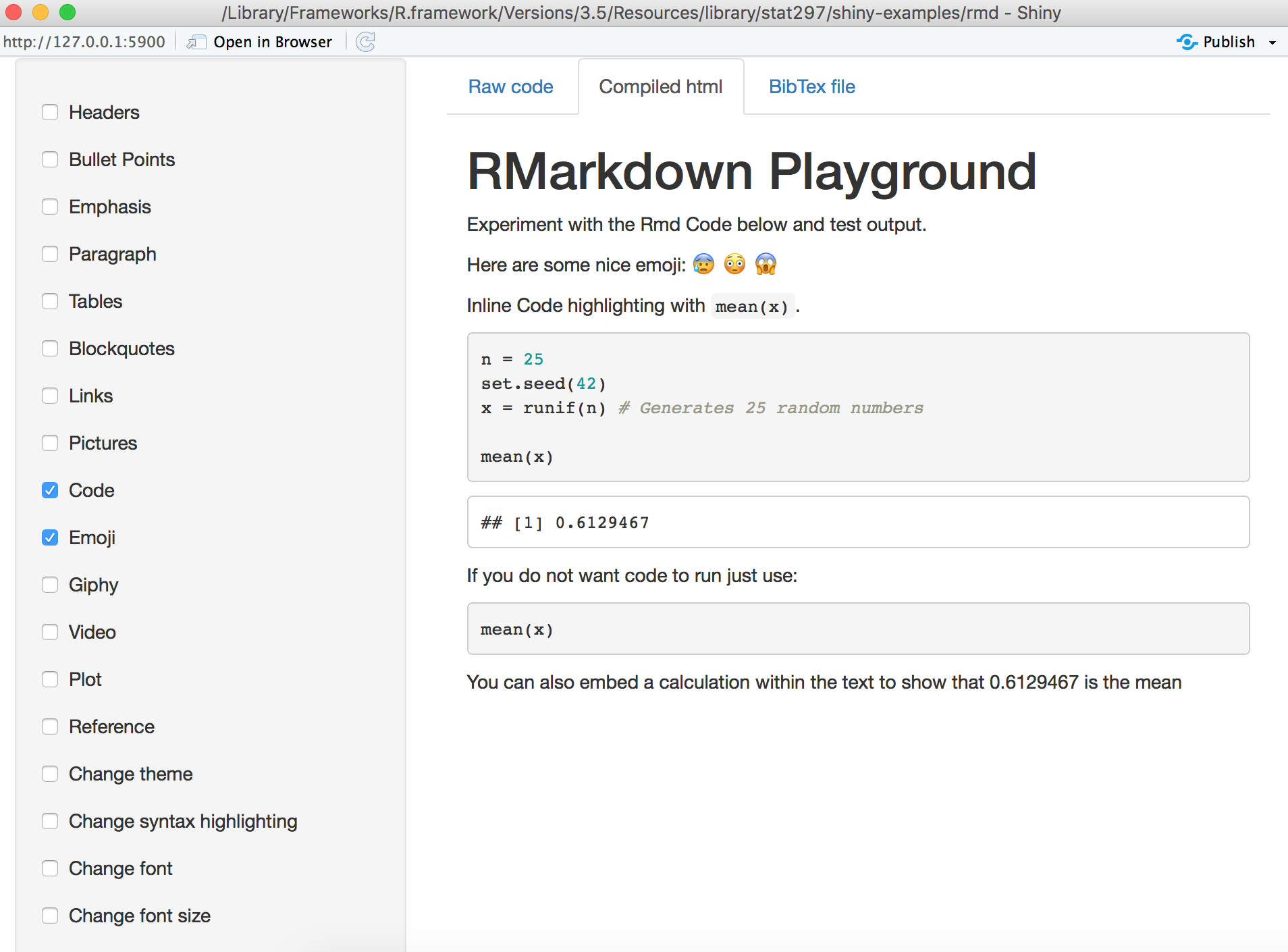

The above code generates the following output:

Now you are ready to experiment different RMarkdown functions and test the corresponding outputs!

You can access either to the web or mobile Rmarkdown app respectively here and here.

Also, the mobile version of the app is embedded below:

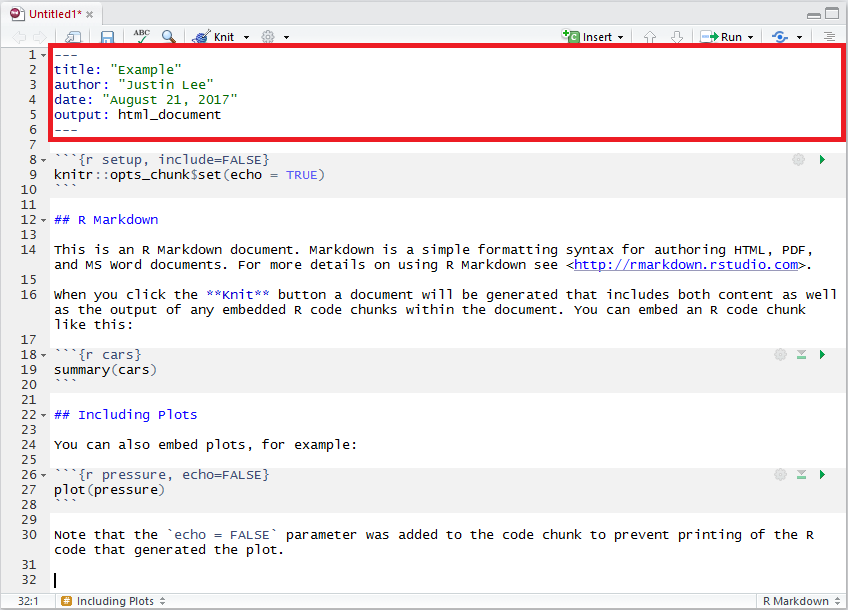

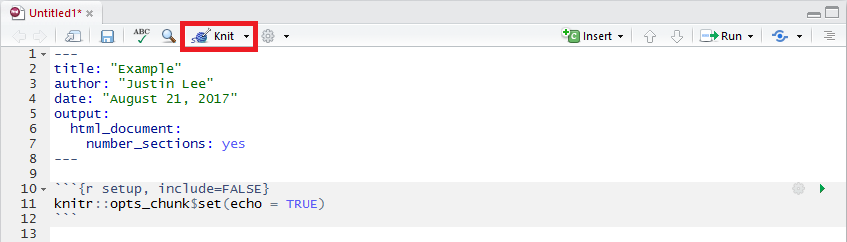

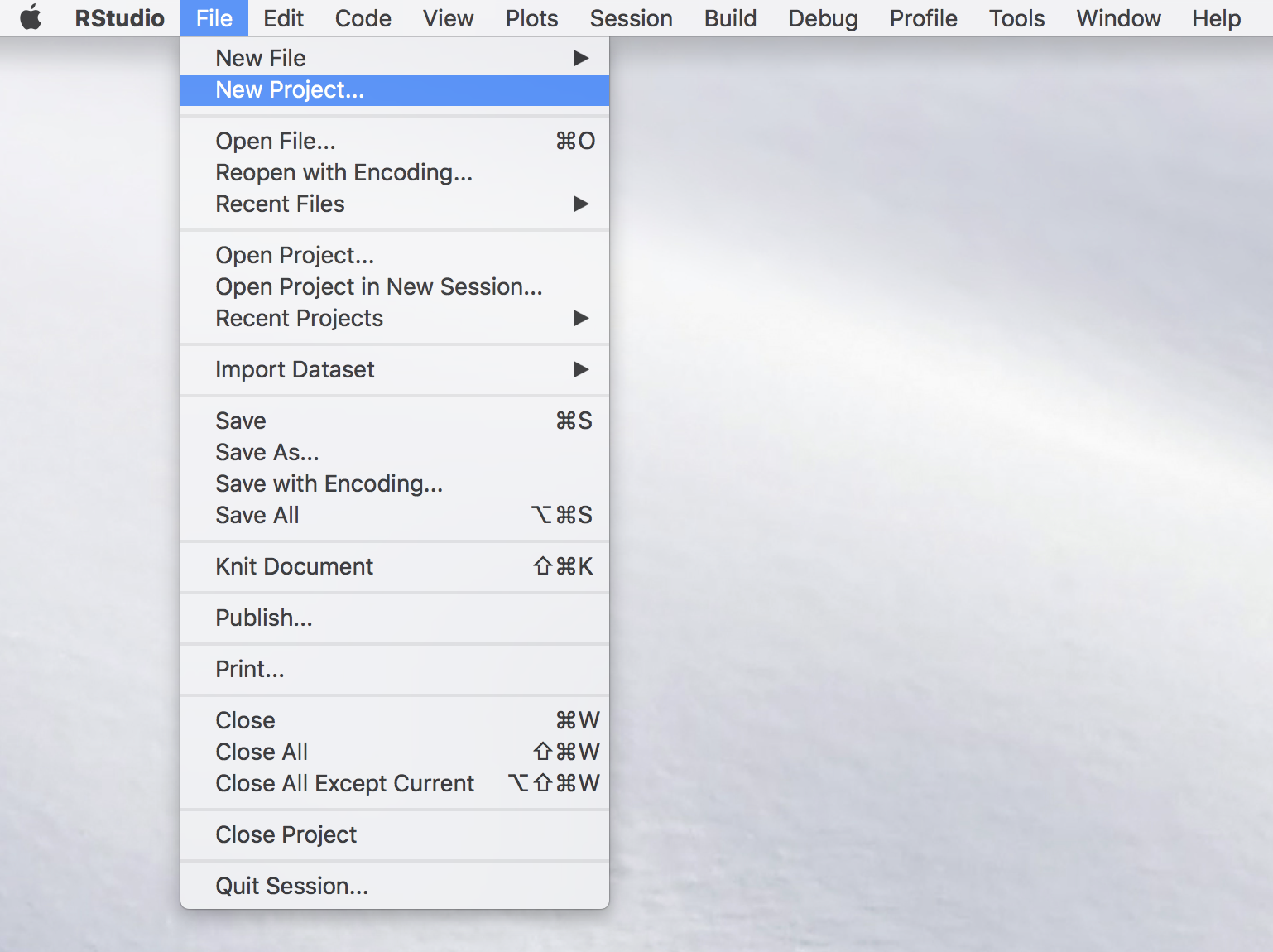

2.1 Create an R Markdown file in RStudio

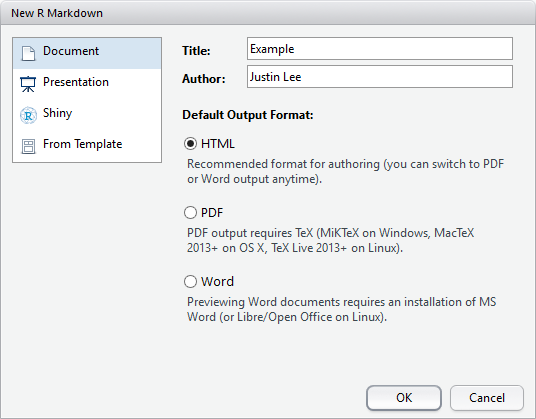

Within RStudio, click File New File R Markdown.

Give the file a title and the author

(your name) and select the default output, HTML.

We can change this later so don’t worry about it for the moment.

An RMarkdown is a plain text file that contains three different aspects:

YAML metadata

Text

Code Chunks

2.2 YAML Metadata

YAML stands for YAML Ain’t Markup Language and is used to specify document configurations and properties such as name, date, output format, etc.

The (optional) YAML header is surrounded before and after by "—" on a dedicated line.

You can also include additional formatting options such as a table of contents or even a custom CSS style template which can be used to further enhance the presentation.

For the purpose of this book, the default options should be sufficient.

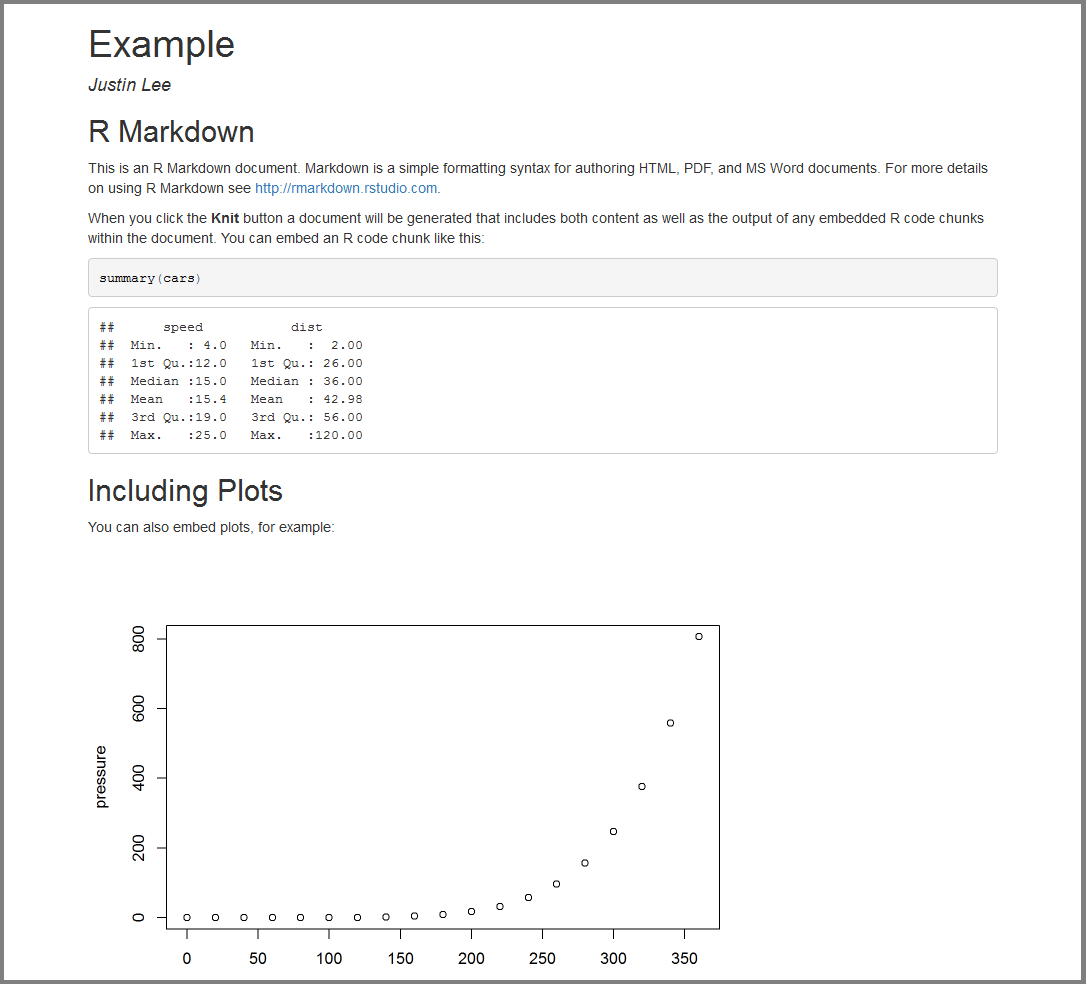

Below is an example knit output of the above RMarkdown file.

The default output above is an html_document format but this format can be modified using, for example, pdf_document to output a pdf.

However, the pdf format requires additional installation and configuration of a TeX distribution such as MikTeX.

Once available, the user can also include raw LaTeX and even define LaTeX macros in the RMarkdown document if necessary (we’ll discuss more about LaTeX further on).

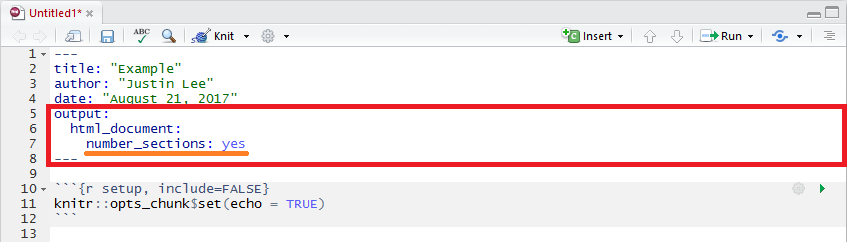

2.2.1 Subsections

To make your sections numbered as sections and subsections, make sure you specify number_sections: yes as part of the YAML Metadata as shown below.

2.3 Text

Due to its literate nature, text will be an essential part in explaining your analysis.

With RMarkdown, we can specify custom text formatting with emphases such as italics, bold, or code style.

To understand how to format text, our previous sentence would be typed out as follows in RMarkdown:

With RMarkdown, we can specify custom text formatting with emphases such as *italics*, **bold**, or `code style

2.3.1 Headers

As seen above, headers are preceded by a #.

A single # produces the largest heading text while, to produce smaller headings, you simply need to add more #s! Heading level also impacts section and subsection nesting in documents and tables of contents, as well as slide breaks in presentation formats.

2.3.2 Lists

Lists can be extremely convenient to make text more readable or to take course notes during class.

RMarkdown allows to create different list structures as shown in the code below:

* You can create bullet points by using symbols such as *, +, or -.

+ simply add an indent or four preceding spaces to indent a list.

+ You can manipulate the number of spaces or indents to your liking.

- Like this.

* Here we go back to the first indent.

1.

To make the list ordered, use numbers.

1.

We can use one again to continue our ordered list.

2.

Or we can add the next consecutive number.

which delivers the following list structure:

You can create bullet points by using symbols such as *, +, or -.

simply add an indent or four preceding spaces to indent a list.

You can manipulate the number of spaces or indents to your liking.

Like this.

Here we go back to the first indent.

To make the list ordered, use numbers.

We can use one again to continue our ordered list.

Or we can add the next consecutive number.

2.3.3 Hyperlinks

To add hyperlinks with the full link, (ex: https://google.com/) you can follow the syntax below:

<https://google.com/>

whereas to add hyperlinks with a custom link title, (ex: Google) follow the syntax below:

[Google](https://google.com)

2.3.4 Blockquotes

Use the > character in front of a line, just like in email to produce blockquotes which styles the text in a way to use if we quote a person, a song or another entity.

"To grow taller, you should shave your head.

Remember to bring the towels!"

Justin Lee

2.3.5 Pictures

To add a picture with captions, follow the syntax below:

which will produce:

Otherwise, to add a picture without any captions, follow the syntax below:

which delivers:

2.3.6 LaTeX

LaTeX is a document preparation system that uses plain text as opposed to formatted text that is used for applications such as Microsoft Word.

It is widely used in academia as a standard for the publication of scientific documents.

It has control over large documents containing sectioning, cross-references, tables and figures.

2.3.6.1 LaTeX in RMarkdown

Unlike a highly formatted word processor, we cannot produce equations by clicking on symbols.

As data scientists there is often the need to explain distributions and equations that are behind the methods we present.

Within the text section of an RMarkdown document you can include LaTeX format text to output different forms of text, mainly equations and mathematical expressions.

Inline mathematical expressions can be added using the syntax: $math expression$.

For example, if we want to write "where (alpha) is in degrees" we would write:

"where $\alpha$ is in degrees".

Using a slightly different syntax (i.e. $$math expression$$) we can obtain centered mathematical expressions.

For example, the binomial probability distribution in LaTeX is written as

$$f(y|N,p) = \frac{N!}{y!(N-y)!}\cdot p^y \cdot (1-p)^{N-y} = {{N}\choose{y}} \cdot p^y \cdot (1-p)^{N-y}$$

which is output as:

\[f(y|N,p) = \frac{N!}{y!(N-y)!}\cdot p^y \cdot (1-p)^{N-y} = {{N}\choose{y}} \cdot p^y \cdot (1-p)^{N-y}\]

An introduction to the LaTeX format can be found here if you want to learn more about the basics.

An alternative can be to insert custom LaTeX formulas using a graphical interface such as codecogs.

2.3.7 Cross-referencing Sections

You can also use the same syntax \@ref(label) to reference sections, where label is the section identifier (ID).

By default, Pandoc will generate IDs for all section headers, e.g., # Hello World will have an ID hello-world.

To call header hello-world as a header, we type \@ref(hello-world) to cross-reference the section.

In order to avoid forgetting to update the reference label after you change the section header, you may also manually assign an ID to a section header by appending {#id} to it.

2.3.8 Citations and Bibliography

Citations and bibliographies can automatically be generated with RMarkdown.

In order to use this feature we first need to create a "BibTex" database which is a simple plain text file (with the extension ".bib") where each reference you would like to cite is entered in a specific manner.

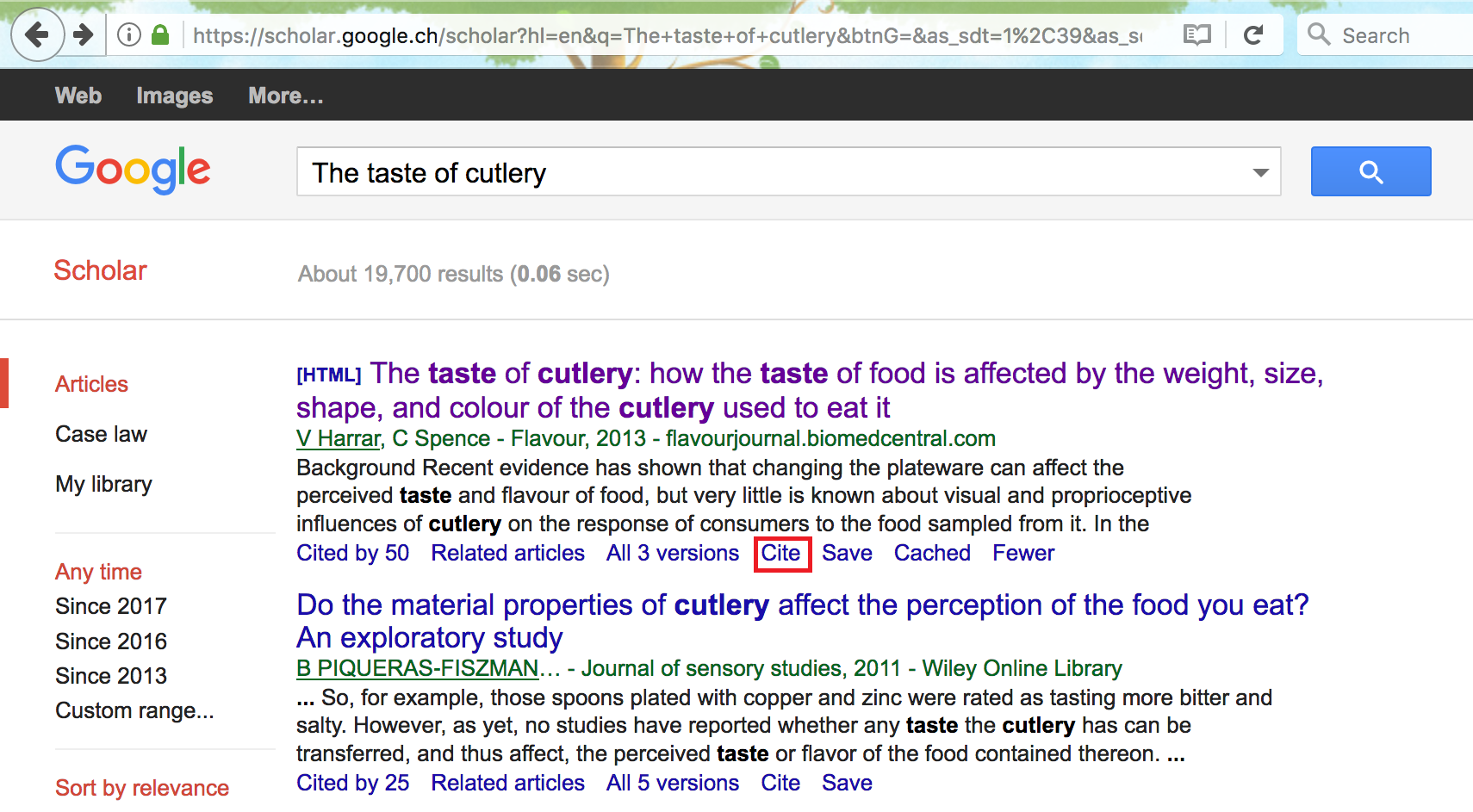

To illustrate how this is done, let us take the example of a recent paper where two researchers from Oxford University investigated the connection between the taste of food and various features of cutlery such as weight and color (calling this phenomenon the "taste of cutlery").

The BibTeX "entry" for this paper is given below:

@article{harrar2013taste,

title={The taste of cutlery: how the taste of food is affected by the weight, size,

shape, and colour of the cutlery used to eat it},

author={Harrar, Vanessa and Spence, Charles},

journal={Flavour},

volume={2},

number={1},

pages={21},

year={2013},

publisher={BioMed Central}

}

This may look like a complicated format to save a reference but there is an easy way to obtain this format without having to manually fill in the different slots.

To do so, go online and search for "Google Scholar" which is a search engine specifically dedicated to academic or other types of publications.

In the latter search engine you can insert keywords or the title and/or authors of the publication you are interested in and find it in the list of results.

In our example we search for "The taste of cutlery" and the publication we are interested in is the first in the results list.

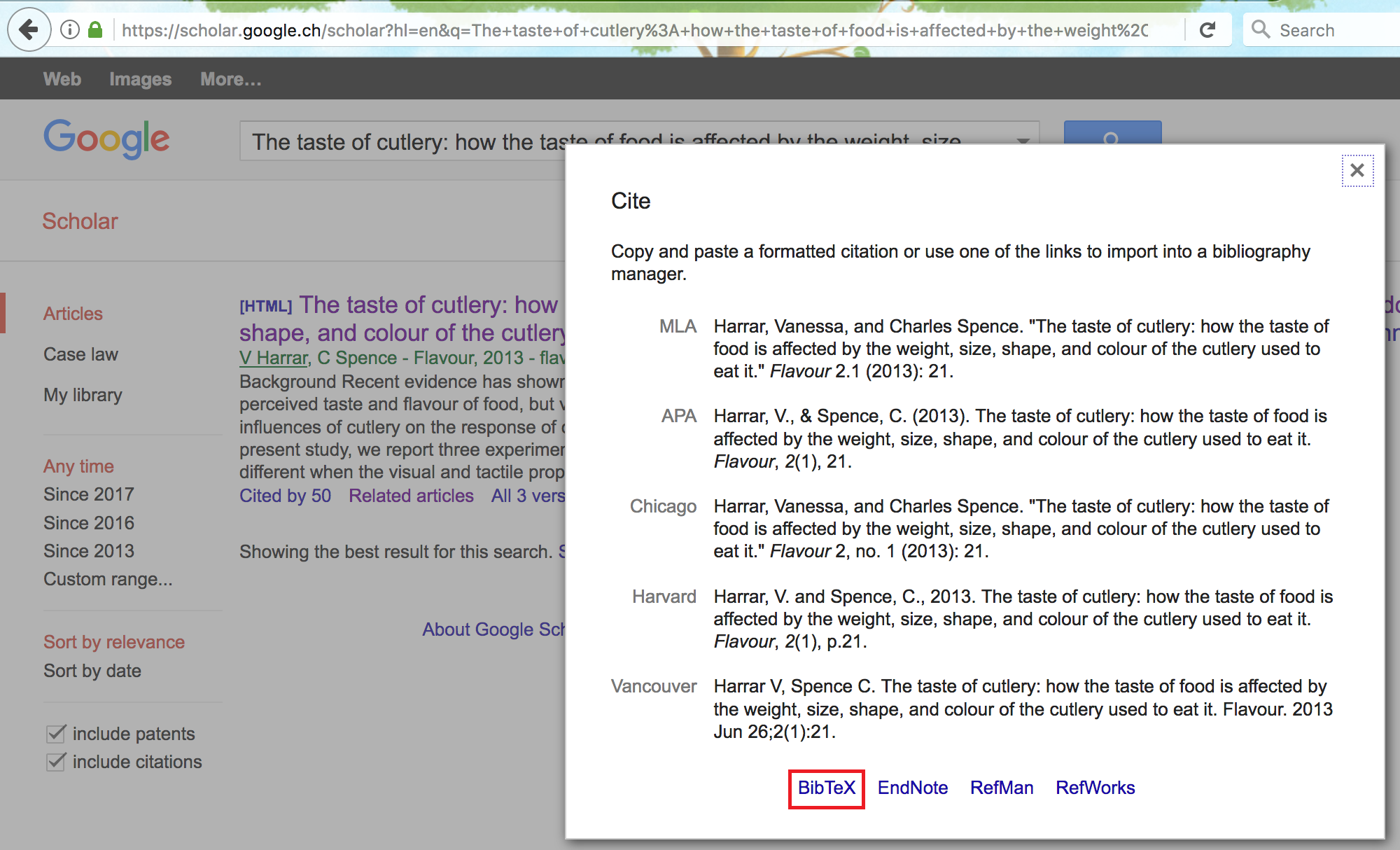

Below every publication in the list there is a set of options among which the one we are interested in is the "Cite" option that should open a window in which a series of reference options are available.

Aside from different reference formats that can be copied and pasted into your document, at the bottom of the window you can find another set of options (with related links) that refer to different bibliography managers.

For ".bib" files we are interested in the "BibTeX" option and by clicking on it we will be taken to another tab in which the format of the reference we want is provided.

All that needs to be done at this point is to copy this format (that we saw earlier in this section) and paste in the ".bib" file you created and save the changes.

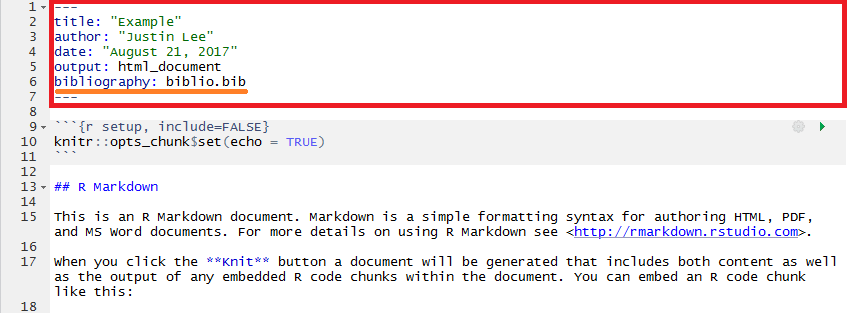

However, your RMarkdown document does not know about the existence of this bibliography file and therefore we need to insert this information in the YAML metadata at the start of our document.

To do so, let us suppose that you named this file "biblio.bib" (saved in the same location as your RMarkdown document).

All that needs to be done is to add another line in the YAML metadata with bibliography: biblio.bib and your RMarkdown will now be able to recognize the references within your ".bib" file.

There are also a series of other options that can be specified for the bibliography such as its format or the way references can be used within the text (see links at the end of this section).

Once the ".bib" file has been created and has been linked to your RMarkdown document through the details in the YAML metadata, you can now start using the references you have collected in the ".bib" file.

To insert these references within your document at any point of your text you need to use the name that starts the reference field in your ".bib" file and place it immediately after the @ symbol (without spaces).

So, for example, say that we wanted to cite the publication on the "taste of cutlery": in your RMarkdown all you have to do is to type @harrar2013taste at the point where you want this citation in the text and you will obtain: Harrar and Spence (2013).

Moreover, it is often useful to put a citation in braces and for example if you want to obtain (see e.g. Harrar and Spence 2013) you can simply write [see e.g.

@harrar2013taste].

The user can also change the name that is used to call the desired reference as long as the same name is used to cite it in the RMarkdown document and that this name is not the same as another reference.

The references in the ".bib" file will not appear in the references that are output from the RMarkdown compiling procedure unless they are specifically used within the RMarkdown document.

Additional information on BibTeX and reference in RMarkdown can be found in the links below:

Introduction to bibtexReference in RMarkdown

2.3.9 Tables

For simple tables, we can be manually insert values as such follows:

+---------------+---------------+--------------------+

| Fruit | Price | Advantages |

+===============+===============+====================+

| *Bananas* | $1.34 | - built-in wrapper |

| | | - bright color |

+---------------+---------------+--------------------+

| Oranges | $2.10 | - cures scurvy |

| | | - **tasty** |

+---------------+---------------+--------------------+

to produce:

Fruit

Price

Advantages

Bananas

$1.34

built-in wrapper

bright color

Oranges

$2.10

cures scurvy

tasty

As an alternative we can use the simple graphical user interface online.

For more extensive tables, we create dataframe objects and project them using knitr::kable() which we will explain later on this book.

2.3.10 Additional References

There are many more elements to creating a useful report using RMarkdown, and we encourage you to use the RMarkdown Cheatsheet as a reference.

2.4 Code Chunks

Code chunks are those parts of the RMarkdown document where it is possible to embed R code within your output.

To insert these chunks within your RMarkdown file you can use the following shortcuts:

the keyboard shortcut Ctrl + Alt + I (OS X: Cmd + Option + I)

the Add Chunk command in the editor toolbar

by typing the chunk delimiters ```{* and ```**.

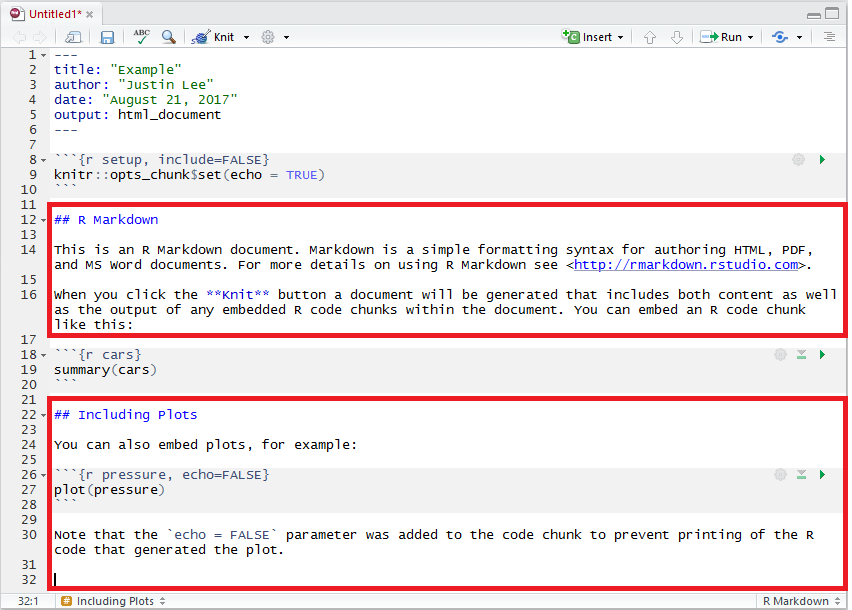

The following example highlights the code chunks in the example RMarkdown document we saw at the start of this chapter:

2.4.1 Code Chunk Options

A variety of options can be specified to manage the code chunks contained in the document.

For example, as can be seen in the third code chunk in the example above, we specify an argument that reads echo = FALSE which is a parameter that was added to the code chunk to prevent printing the R code that generated the plot.

This is a useful way to embed figures.

More options can be found from the RMarkdown Cheatsheet and Yihui’s notes on knitr options.

Here are some explanations of the most commonly used chunk options taken from these references:

eval: (TRUE; logical) whether to evaluate the code chunk;

echo: (TRUE; logical or numeric) whether to include R source code in the output file;

warning: (TRUE; logical) whether to preserve warnings (produced by warning()) in the output like we run R code in a terminal (if FALSE, all warnings will be printed in the console instead of the output document);

cache: (FALSE; logical) whether to "cache" a code chunk.

This option is particularly important in practice and is discussed in more details in Section 2.4.4.

Plot figure options:

fig.path: (‘figure/’; character) prefix to be used for figure filenames (fig.path and chunk labels are concatenated to make filenames);

fig.show: (‘asis’; character) how to show/arrange the plots;

fig.width, fig.height: (both are 7; numeric) width and height of the plot, to be used in the graphics device (in inches) and have to be numeric;

fig.align: (‘default’; character) alignment of figures in the output document (possible values are left, right and center;

fig.cap: (NULL; character) figure caption to be used in a figure environment.

2.4.2 Comments

Adding comments to describe the code is extremely useful (if not essential) during every coding and programming process.

It helps you take notes and remember what is going on and why you made use of these functions, as well as helping others understand your code.

Forgetting to comment or document your code often becomes a larger problem in the future when, among numerous lines of code, you have forgotten the reason for using certain functions or algorithms.

"Don’t document bad code – rewrite it."

The Elements of Programming Style, Kernighan & Plauger

# Comment your code by preceding text with a #

# Keep it brief but comprehensible, so you can return to it

2.4.3 In-line R

The variables we store in an RMarkdown document will stay within the environment they were created in.

This means that we can call and manipulate them anywhere within the document.

For example, supposing we have a variable called x to which we assign a specific value, then in RMarkdown we can reference this variable by using r x: this will affix the value of the variable directly in a sentence.

Here is a practical example:

a = 2

where we have stored the value 2 in a variable called a.

We can use the value of a as follows:

The value of $a$ is `r a`.

This translates in R Markdown to "The value of (a) is 2."

2.4.4 Cache

Depending on the complexity of calculations in your embedded R code, it may be convenient to avoid re-running the computations (which could be lengthy) each time you knit the document together.

For this purpose, it possible to specify an additional argument for your embedded R code which is the cache argument.

By default this argument is assigned the value FALSE and therefore the R code is run every time your document is compiled.

However, if you specify this argument as cache = TRUE, then the code is only run the first time the document is compiled while the following times it simply stores and presents the results of the computations when the document was first compiled.

Below is a short video introducing caching in R Markdown.

The RMarkdown file used for this particular example can be found here: caching.Rmd.

Let us consider an example where we want to embed an R code with a very simple operation such as assigning the value of 2 to an object that we call a (that we saw earlier).

This is clearly not the best example since this operation runs extremely quickly and there is no visible loss in document compilation time.

However, we will use it just to highlight how the cache argument works.

Therefore, if we want to avoid running this operation each time the document is compiled, then we just embed our R code as follows:

a = 2

which would be written in RMarkdown as:

```{r computeA, cache = TRUE}

a = 2

```

You will notice that we called this chunk of embedded R code computeA and the reason for this will become apparent further on.

Once we have done this we can compile the document that will run this operation and store its result.

Now, if we compile the document again (independently from whether we made changes to the rest of the document or not) this operation will not be run and the result of the previous (first) compiling will be presented.

However, if changes are made to the R code which has been "cached", then the code will be run again and this time its new result will be stored for all the following compilings until it is changed again.

This argument can therefore be very useful when computationally intensive R code is embedded within your document.

Nevertheless it can suffer from a drawback which consists in dependencies of your "cached" R code with other chunks within the document.

In this case, the other chunks of R code can be modified thereby outputting different results but these will not be considered by your "cached" R code.

As an example, suppose we have another chunk of R code that we can "cache" and that takes the value of a from the previous chunk:

(d = 2*a)

## [1] 4

which would be written in RMarkdown as:

```{r, cache = TRUE}

(d = 2*a)

```

In this case, the output of this chunk will be ## 4 since a = 2 (from the previous chunk).

What happens however if we modify the value of a in the previous chunk? In this case, the previous chunk will be recomputed but the value of d (in the following chunk) will not be updated since it has stored the value of 4 and it is not recomputed since this chunk has not been modified.

To avoid this, a solution is to specify the chunks of code that the "cached" code depends on.

This is why we initially gave a name to the first chunk of code ("computeA") so as to refer to it in following chunks of "cached" code that depend on it.

To refer to this code you need to use the option dependson as follows:

(d = 2*a)

## [1] 4

which we would write as:

```{r, cache = TRUE, dependson = "computeA"}

(d = 2*a)

```

In this manner, if the value of a changes in the first chunk, the value of d will also change but will be stored until either the computeA chunk or the latter chunk is modified.

2.5 Render Output

After you are done, run RMarkdown::render() or click the Knit button at the top of the RStudio scripts pane to save the output in your working directory.

The use of RMarkdown makes it possible to generate any file format such as HTML, pdf and Word processor formats using pandoc.

Pandoc is a free software that understands and converts useful markdown syntax, such as the code mentioned above, into a readable and clean format.

git gets easier once you get the basic idea that branches are homeomorphic endofunctors mapping submanifolds of a Hilbert space.

Isaac Wolkerstorfer

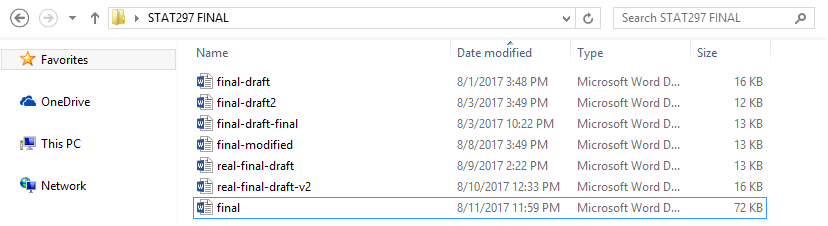

When working on a report or a project, it is often the case that you keep separate versions either to keep track of the changes (in case you want to go back to a previous version) or to have a version for each person working on different parts of the project.

As a result of this approach, you may have created or encountered a file directory attempting to preserve multiple copies or iterations of the same files:

This behavior is basically a defensive strategy attempting to remedy one or more a real or percieved threats to progress.

For example,

you or a collaborator may have made progress on different parts of the project in separate versions of the document

you may want to preserve an earlier state of the document (e.g. a "clean" copy before proposing edits)

Unforutunately, this type of strategy can easily lead to frustration as users lose track of which documents have the most up-to-date content for different portions of the document.

This is effectively a problem of "version control" (sometimes called "source control").

To respond to this problem, software has been developed to keep track of your changes by informing you on the saves you made and allowing you to go back to previous versions in order to revert those changes.

This chapter discusses the features of this software as well as introducing a specific version control tools: Git and GitHub.

People often use the two somewhat interchangeably in casual discussion–or use GitHub as a surrogate for the combination.

In fact, Git is the name of the version control software, and everything that Git can accomplish is possible to do without using GitHub at all.

GitHub is a commercial web-based version control repository hosting service which includes some additional features to make Git more user-friendly.

3.1 Version Control

As mentioned above, version control is a system that records changes to a file or a set of files in order to keep track and possibly revert to or modify those changes over time.

More specifically, it allows you to:

record the entire history of a file;

revert to a specific version of the file;

collaborate on the same platform with other people;

make changes without modifying the main file and add them once you feel comfortable with them.

All these features are highly important when projects start becoming more complex and/or include multiple contributors.

There are several mature software tools designed for version control including, but not limited to, Git, Subversion, Mercurial, and more.

Furthermore, there are several web-based version control repository hosting services such as GitLab, GitHub, Bitbucket, and more that accomplish the same goals.

In the next section, we introduce use of Git and GitHub as tools for version control and collaboration.

Rather than save many independent copies of each file–as shown earlier when the user saved many versions of a "final" document–most version control software tools simply track incremental changes to the files under version control.

Storing a complete record of just the bits that change from one version to the next is far more efficient than saving many copies of whole documents for which a majority of the content may be unchanged from one iteration to the next.

Moreover, with a complete record of every incremental change, it’s just as easy to piece together the current state of a document or to rebuild a previous the state of a document at an earlier point recorded in it’s development lifecycle.

In other words, it’s like version control software effectively offers access to free a document editing time machine!

3.2 Git and GitHub

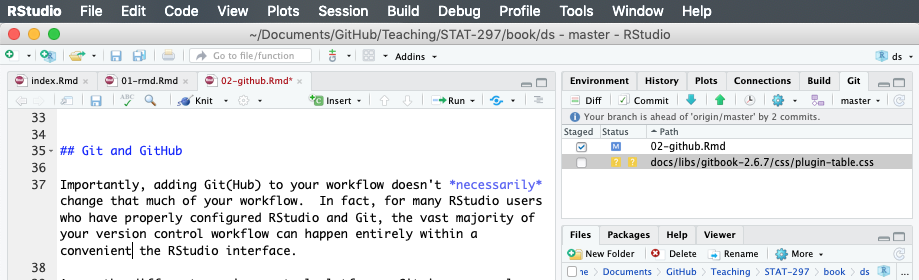

Importantly, adding Git(Hub) to your workflow doesn’t necessarily change that much of your workflow.

In fact, for many RStudio users who have properly configured RStudio and Git, the vast majority of your version control workflow can happen entirely within a convenient the RStudio interface.

We’ll discuss specific details, but it’s sufficient to note the "Git" tab shown in the upper right pane of the RStudio window shown.

The latter uses the Git platform and stores local files into a flexible folder called a "repository".

Git(Hub) uses repositories to organize your work.

If you like, you can store a bunch of files in a repository (or Repo) on the GitHub remote servers and delete them from your computer entirely.

You can replace the files with new versions or even edit some specific types of files right from the GitHub webpage.

When you are ready to get them back, you could simply locate the files through your GitHub account and retrieve them.

More commonly, users establish a link between a file directory on their (local) computer and a Repo stored on the GitHub remote.

You edit files on your computer and save your progress as you normally would, except now that you have established a link with Git(Hub) you can periodically update the Repo on the GitHub remote with the latest progress.

Below is a video introducing the basic look and feel of GitHub.

3.2.1 Git & RStudio Configuration

As mentioned previously, with proper configuration a large majority of your use of Git can happen entirely within the RStudio environment.

In this section, we step through a basic configuration.

If necessary, a more comprehensive guide to configuring Git(Hub) and R/RStudio is available at https://happygitwithr.com/ from which a substantial portion of this congifiguration guidance was originally adapted.

3.2.1.1 Install Git

Before begining, make sure you have installed both R and RStudio.

Some systems will already have Git installed, or will install Git automatically when prompted.

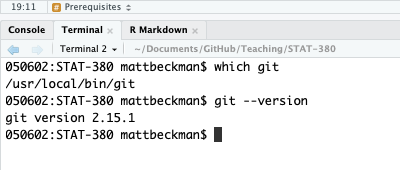

In either case, open a terminal in RStudio (RStudio >> Tools >> Terminal >> New Terminal) and then enter the following commands–one at a time–after the dollar sign prompt ($) as shown below.

which git

git --version

If git is installed, the result will indicate a where the software is located and the version you have available.

If Git has not yet been installed, go to the website and select the version which is compatible with the OS of your computer (e.g. Windows/Mac/Linux/Solaris).

Again, for additional support corresponding to various operating systems see https://happygitwithr.com/install-git.html.

3.2.1.2 Tell Git Who You Are

Once Git is installed, the first thing you should do is set your name and the email address associated with your GitHub profile.

This is information is used to synchronize the work on your computer with your Repo on the GitHub remote server.

Again, you will need a Terminal window in RStudio (RStudio >> Tools >> Terminal >> New Terminal) and then enter the following commands–one at a time–after the dollar sign prompt ($) as shown below.

git config --global user.name 'Aaron Carlson'

git config --global user.email 'abc1234@psu.edu'

git config --global --list

Note: the last command git config --global --list should verify that Git now knows you! …or at least acknowledges your name and email address.

This operation only needs to be done once when using the "–global" option because, in this case, Git will always use that information for anything you do on that system.

If you want to override this with a different name or email address for specific projects, you can run the command without the "–global" option while working on those projects.

3.2.2 GitHub Setup

In order to set up GitHub, go to the GitHub website and, for the purposes of the course, the first step is to sign up with your University email address.

Your username and email can be changed at any time so, if you want to change it, you can easily do so after the course.

Your GitHub profile can also serve as a resume of your data science skills that will be highlighted by possible future projects that you save and commit.

Since your profile will be public, it’s a good idea to choose a username that you would be comfortable sharing with an employer in a job interview.

Better still is a name that is recognizable as you as a derivative of your actual name.

For example, our sample name in the last section, Aaron Carlson, might choose "acarlson" as a username rather than "abc1234" which would not be recognizable to those outside the university.

Once you have a GitHub profile, log in and create a Repo for your project (or navigate to an existing Repo).

Make sure you check the box to "initialize this repository with a README." It’s generally a good idea to always initialize new Repos with a README unless you have a specific reason not to do so. Then, click the green button "Clone or Download" and copy the URL as shown here.

3.2.3 Connecting to RStudio

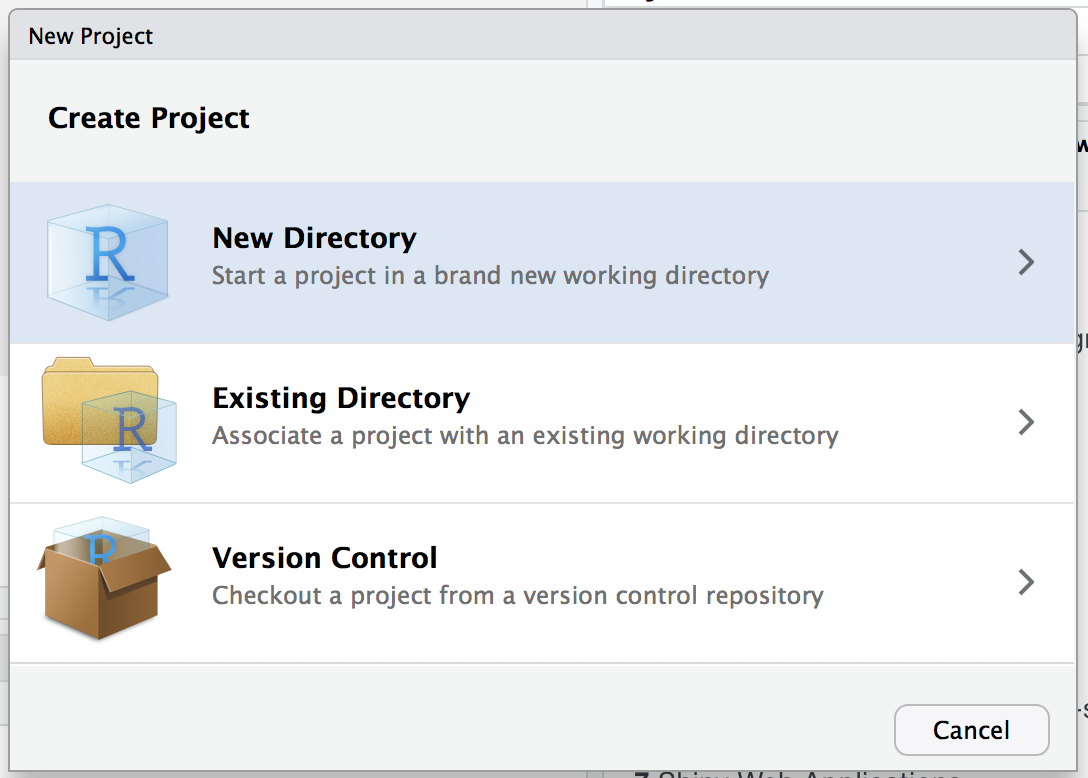

With the URL of your GitHub Repo still copied to your clipboard, go to RStudio and initate a new "Project." You can either navigate the menus in RStudio (RStudio >> File >> New Project) or use the "Project" navigation feature in the upper right of the RStudio window a shown.

Next, RStudio will prompt you with a dialogue box to configure the new project.

Select "Version Control" and then "Git" on the following screen as shown.

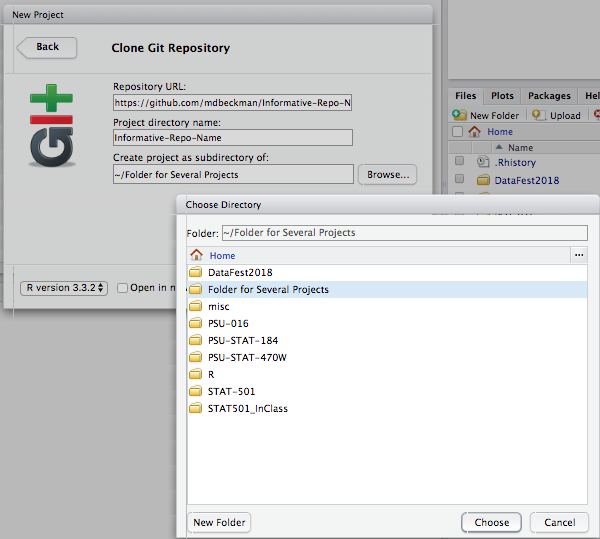

Remember when you copied the URL for your Repo from GitHub? If not, go copy it again and we’ll paste it into the line "Repository URL" in order to "Clone" the Git Repository to a file directory (i.e. folder) on your computer as shown.

"Repository URL": Paste the URL that you previously copied from GitHub

"Project Directory Name": This will be the name of a new folder (i.e. directory) on your computer.

Use the same name as your GitHub Repo (e.g. mine was "Informative-Repo-Name" here).

"Create Project as a Subdirectory Of": This is the location on your computer for the new folder.

For example, you may want to make a folder on your computer for each class and then put this Repo (and others for the class) together in that directory location.

You’re in! (hopefully)…

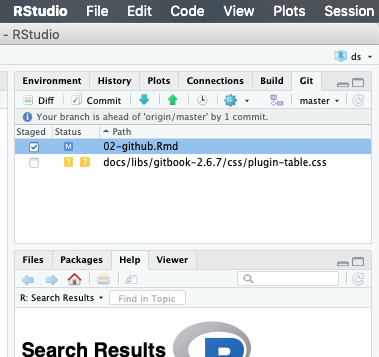

The "Project" menu shown in the upper right corner of the RStudio Server Window now shows the name of your Repo/Project (e.g. mine was "Informative-Repo-Name" in this demonstration).

Also, a new "Git" tab appears and has started tracking file changes in my Repo.

A few initial files will appear (e.g., ".gitignore" and something ending in ".RProj").

These basically help Git & RStudio handle logistics, just "commit" and "push" them.

From now on, nearly everything (~90-95%) of your interactions with Git can happen in RStudio… at least in this class.

The remaining bits consist of things like initializing or cloning Repos from the GitHub website.

If you do internet searches for Git help, you’ll see lots of command line terminal stuff, but you won’t likely need to execute commands in the terminal for our purposes.

The basic workflow is as follows…

Open the RStudio Project connected to your Git(Hub) Repo

Work on your computer just like always

Save your work often just like always

When you want to preserve a snapshot of your project, you make a "commit"

When you have a few commits and want to archive them, you "push" them to the GitHub remote server

If you decide to work from a different computer, or want to pick up where a collaborator left off, you can "pull" the most up-to-date version of the files from the GitHub remote to your local computer and go back to step 2.

Let’s unpack the workflow slightly…

Open the RStudio Project connected to your Git(Hub) Repo. We’ll come back to this when we discuss common mistakes.

Work on the files just like you always do. Seriously.

This certainly includes technical tasks like writing code in R, but it also includes standard operations like dragging and dropping things into the directory folder linked to your Repo.

For example, if you want to have access to a picture or a file with a data set in it, you could copy it to the directory folder for your project just like you normally would.

When you add a new file, you may simply notice the name of that file will appear on a list in the "Git" tab in your RStudio window.

Git is basically just alerting you that it has noticed something changed in the repo, that’s all.

Save your work often just like always.* You should save your work as you make progress just like you always would, even if Git weren’t involved.

When you save changes to an existing file, the name of that file will appear on a list in the "Git" tab in your RStudio window again.

Once again, Git is just alerting you that it has noticed something changed.

Git is very observant that way.

When you want to preserve a snapshot of your project, you make a "commit." This is the first new bit.

A commit is quite literally a snapshot of the state of your whole project (e.g., file directory), like a photograph.

One you take a photograph, you have an exact picture of precisely how things looked at that moment in time.

You should make commits frequently as you make progress with your work.

When you want to make a commit using the RStudio interface, you simply select a small checkbox next to the files that you want to include in the snapshot.

This is called "staging" files for the commit.

Then, when you click the "commit button, a new window will open that will attempt to summarize all the differences between the new file and the previous version.

This is called the"diff."

In order to complete each commit, you must include a commit message.

It’s a good idea to write informative commit messages, and Git will even force you to write something before executing the commit.

Remember when we described version control as a sort of time machine? You will probably be the one reading through many dozens of commit messages to figure out where to send the time machine… They are also tremendously helpful if you have collaborators on a Repo so you can all keep up with what is changing throughout the project.1

When you have a few commits and want to archive them, you "push" them to the GitHub remote server.

This is the first step in the workflow that is not simply happening on your local computer.

When you "push" one or more commits to the GitHub remote server it is like archiving all of those snapshots/photographs in a permanent file cabinet.

If you decide to work from a different computer, or want to pick up where a collaborator left off, you can "pull" the most up-to-date version of the files from the GitHub remote to your local computer and go back to step 2.

Again, nearly everything you are doing with Git is happening locally on your computer.

If a collaborator made changes on a different computer, or if you made changes from a different computer somewhere, you will need to "pull" them from the GitHub remote into your local working directory.

Actually, if you are working from several computers or with other collaborators, it’s a good habit to "pull" before you "push" in order to make sure that you don’t end up with two different versions of the same thing that are in direct conflict with one another.

This results in a "merge conflict" and can become a bit of a headache to untangle.

3.2.4.1 Common mistakes in the Git/RStudio Workflow

Commits in the wrong Repo.

It’s a common mistake to forget to change from one RStudio Project to the next.

If you forget, it may look like your changes aren’t tracked by Git.

In reality, Git will still monitor changes… but it is monitoring them in the correct Repo linked to the file, so you won’t be able to make commits on those files until you change to the correct RStudio Project.

Large files.

GitHub is generously storing all sorts of things for us and (as academic users) doing so free of charge.

Having said that, storage presumably costs them money, so they don’t like to store large files.

You’ll be warned if you try and commit any single file that is more than 10 MB.

There are sensible ways to work around this, but a common strategy is to tell Git to simply "ignore" the large file… that is, don’t include it in my snapshots and don’t archive it on the GitHub remote.

3.2.5 Note about GitHub Student Developer Pack

As a student, it is possible to benefit from specific advantages when using GitHub.

Indeed, once you have set up your profile you can go to this link and follow the steps below to set up a "student developer pack" discount request to GitHub.

Through this setup it will be possible for you not only to have unlimited free public repositories.

In the past, students could access free unlimited private repositories only after some vetting by GitHub.

This changed in 2019 shortly after GitHub was acquired by Microsoft.

At the time of this writing, free unlimited private repositories were made available to all users, and restrictions were instead based on limiting the number of collaborators for private Repos.

Students should still get the student developer pack, but it may not be as critical as it once was for most student users.

3.3 Issues

Issues are a very good way to keep track of group tasks, bugs and announcements for your projects within GitHub.

Below is a basic video introducing issues in GitHub.

3.4 Slack Integration

Slack is a platform created to communicate between group members, allowing for both direct individual messages as well as group messages.

More information on how to use Slack can be found in this Slack Tutorial.

An added benefit of using Slack is that it can be integrated with GitHub in such a way that notifications will be posted to the group whenever someone pushes or makes a pull request.

More information on GitHub integration with Slack can be found here.

A more detailed video providing a demonstration on the use of Slack in a real-life setting can be found below.

3.5 Additional References

Below are some supplemental references that can support you in a better use of GitHub.

http://happygitwithr.com/

Chapter 4 Data Structures

There are different data types that are commonly used in R among which the most important ones are the following:

Numeric (or double): these are used to store real numbers.

Examples: -4, 12.4532, 6.

Integer: examples: 2L, 12L.

Logical (or boolean): examples: TRUE, FALSE.

Character: examples: "a", "Bonjour".

In R there are five types of data structures in which elements can be stored.

A data structure is said to homogeneous if it only contains elements of the same type (for example it only contains character or only numeric values) and heterogenous if it contains elements of more than one type.

The five types of data structures are commonly summarized in a table similar to the one below (see e.g. Wickham 2014a):

Table 4.1: Five most common types of data structures used in R (Wickham 2014a).

Dimension

Homogenous

Heterogeneous

1

Vector

List

2

Matrix

Data Frame

n

Array

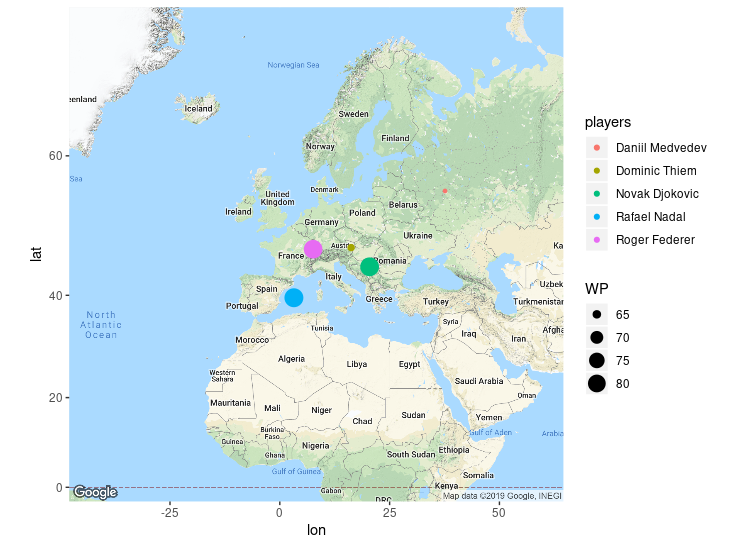

Consider a simple data set of the top five male single tennis players presented below:

Table 4.2: Five best male single tennis players as ranked by ATP (09-30-2019).

Name

Date of Birth

Place of Birth

Place of Residence

ATP Ranking

Prize Money

Win Percentage

Grand Slam Wins

Pro Since

Novak Djokovic

22 May 1987

Belgrade, Serbia

Monte Carlo, Monaco

1

135,259,120

82.7

16

2003

Rafael Nadal

3 June 1986

Manacor, Spain

Manacor, Spain

2

115,178,858

83.1

19

2001

Roger Federer

8 August 1981

Basel, Switzerland

Wollerau, Switzerland

3

126,840,700

82.2

20

1998

Daniil Medvedev

11 February 1996

Moscow, Russia

Monte Carlo, Monaco

4

8,171,483

63.6

0

2014

Dominic Thiem

3 September 1993

Wiener Neustadt, Austria

Lichtenwörth, Austria

5

18,588,662

64.3

0

2011

Notice that this data set contains a variety of data types; in the next sections we will use this data to illustrate how to work with five common data structures.

4.1 Vectors

A vector has three important properties:

The Type of objects contained in the vector.

The function typeof() returns a description of the type of objects in a vector.

The Length of a vector indicates the number of elements in the vector.

This information can be obtained using the function length().

Attributes are metadata attached to a vector.

The functions attr() and attributes() can be used to store and retrieve attributes (more details can be found in Section 4.1.4).

c() is a generic function that combines arguments to form a vector.

All arguments are coerced to a common type (which is the type of the returned value) and all attributes except names are removed.

For example, consider the number of grand slams won by the five players considered in the eighth column of Table 4.2:

grand_slam_win = c(16, 19, 20, 0, 0)

To display the values stored in grand_slam_win we could simply enter the following in the R console:

grand_slam_win

## [1] 16 19 20 0 0

Alternatively, we could have created and displayed the value by using () around the definition of the object itself as follows:

(grand_slam_win = c(16, 19, 20, 0, 0))

## [1] 16 19 20 0 0

Various forms of "nested concatenation" can be used to define vectors.

For example, we could also define grand_slam_win as

(grand_slam_win = c(16, c(19, 20, c(0, c(0)))))

## [1] 16 19 20 0 0

This approach is often used to assemble vectors in various ways.

It is also possible to define vectors with characters, for example we could define a vector with the player names as follows:

(players = c("Novak Djokovic", "Rafael Nadal", "Roger Federer",

"Daniil Medvedev", "Dominic Thiem"))

## [1] "Novak Djokovic" "Rafael Nadal" "Roger Federer"

## [4] "Daniil Medvedev" "Dominic Thiem"

4.1.1 Type

We can evaluate the kind or type of elements that are stored in a vector using the function typeof().

For example, for the vectors we just created we obtain:

typeof(grand_slam_win)

## [1] "double"

typeof(players)

## [1] "character"

This is a little surprising since all the elements in grand_slam_win are integers and it would seem natural to expect this as an output of the function typeof().

This is because R considers any number as a "double" by default, except when adding the suffix L after an integer.

For example:

typeof(1)

## [1] "double"

typeof(1L)

## [1] "integer"

Therefore, we could express grand_slam_win as follows:

(grand_slam_win_int = c(16L, 19L, 20L, 0L, 0L))

## [1] 16 19 20 0 0

typeof(grand_slam_win_int)

## [1] "integer"

In general, the difference between the two is relatively unimportant.

4.1.2 Coercion

As indicated earlier, a vector has a homogeneous data structure meaning that it can only contain a single type among all the data types.

Therefore, when more than one data type is provided, R will coerce the data into a "shared" type.

To identify this "shared" type we can use this simple rule:

\[\begin{equation*}

\text{logical} < \text{integer} < \text{numeric} < \text{character},

\end{equation*}\]

which simply means that if a vector has more than one data type, the "shared" type will be that of the "largest" type according to the progression shown above.

For example:

# Logical + numeric

(mix_logic_int = c(TRUE, 12, 0.5))

## [1] 1.0 12.0 0.5

typeof(mix_logic_int)

## [1] "double"

# Numeric + character

(mix_int_char = c(14.3, "Hi"))

## [1] "14.3" "Hi"

typeof(mix_int_char)

## [1] "character"

4.1.3 Subsetting

Naturally, it is possible to "subset" the values of in our vector in many ways.

Essentially, there are four main ways to subset a vector.

Here we’ll only discuss the first three:

Positive Index: We can access or subset the (i)-th element of a vector by simply using grand_slam_win[i] where (i) is a positive number between 1 and the length of the vector.

# Accessing the first element

grand_slam_win[1]

## [1] 16

# Accessing the third and first value

grand_slam_win[c(3, 1)]

## [1] 20 16

# Duplicated indices yield duplicated values

grand_slam_win[c(1, 1, 2, 2, 3, 4)]

## [1] 16 16 19 19 20 0

Negative Index: We remove elements in a vector using negative indices:

# Removing the second observation

grand_slam_win[-2]

## [1] 16 20 0 0

# Removing the first and fourth observations

grand_slam_win[c(-1, -4)]

## [1] 19 20 0

Logical Indices: Another useful approach is based on logical operators:

# Access the first and fourth observations

grand_slam_win[c(TRUE, FALSE, FALSE, TRUE, FALSE)]

## [1] 16 0

Note that it is not permitted to "mix" positive and negative indices.

For example, grand_slam_win[c(-1, 2)] would produce an error message.

4.1.4 Attributes

Let’s suppose that we conduct an experiment under specific conditions, say a date and place that are stored as attributes of the object containing the results of this experiment.

Indeed, objects can have arbitrary additional attributes that are used to store metadata on the object of interest.

For example:

attr(grand_slam_win, "date") = "09-30-2019"

attr(grand_slam_win, "type") = "Men, Singles"

To display the vector with its attributes

grand_slam_win

## [1] 16 19 20 0 0

## attr(,"date")

## [1] "09-30-2019"

## attr(,"type")

## [1] "Men, Singles"

To only display the attributes we can use

attributes(grand_slam_win)

## $date

## [1] "09-30-2019"

##

## $type

## [1] "Men, Singles"

It is also possible to extract a specific attribute

attr(grand_slam_win, "date")

## [1] "09-30-2019"

4.1.5 Adding Labels

In some cases, it is useful to characterize vector elements with labels.

For example, we could define the vector grand_slam_win and associate the name of each corresponding athlete as a label, i.e.

(grand_slam_win = c("Novak Djokovic" = 16, "Rafael Nadal" = 18,

"Roger Federer" = 20, "Daniil Medvedev" = 0,

"Dominic Thiem" = 0))

## Novak Djokovic Rafael Nadal Roger Federer Daniil Medvedev

## 16 18 20 0

## Dominic Thiem

## 0

The main advantage of this approach is that the number of grand slams won can now be referred to by the player’s name.

For example:

grand_slam_win["Novak Djokovic"]

## Novak Djokovic

## 16

grand_slam_win[c("Novak Djokovic","Roger Federer")]

## Novak Djokovic Roger Federer

## 16 20

All labels (athlete names in this case) can be obtained with the function names(), i.e.

names(grand_slam_win)

## [1] "Novak Djokovic" "Rafael Nadal" "Roger Federer"

## [4] "Daniil Medvedev" "Dominic Thiem"

4.1.6 Working with Dates

When working with dates it is useful to treat them as real dates rather than character strings that look like dates (to a human) but don’t otherwise behave like dates.

For example, consider a vector of three dates: c("03-21-2015", "12-13-2011", "06-27-2008").

The sort() function returns the elements of a vector in ascending order, but since these dates are actually just character strings that look like dates (to a human), R sorts them in alphanumeric order (for characters) rather than chronological order (for dates):

# The `sort()` function sorts elements in a vector in ascending order

sort(c("03-21-2015", "12-31-2011", "06-27-2008", "01-01-2012"))

## [1] "01-01-2012" "03-21-2015" "06-27-2008" "12-31-2011"

Converting the character strings to "yyyy-mm-dd" would solve our sorting problem, but perhaps we also want to calculate the number of days between two events that are several months or years apart.

The as.Date() function is one straight-forward method for converting character strings into dates that can be used as such.

The typical syntax is of the form:

as.Dates(<vector of dates>, format = <your format>)

Considering the dates of birth presented in Table 4.2 we can save them in an appropriate format using:

(players_dob = as.Date(c("22 May 1987", "3 Jun 1986", "8 Aug 1981",

"11 Feb 1996", "3 Sep 1993"),

format = "%d %b %Y"))

## [1] "1987-05-22" "1986-06-03" "1981-08-08" "1996-02-11" "1993-09-03"

Note the syntax of format = "%d %b %Y".

The following table shows common format elements for use with the as.Date() function:

Table 4.3: Common date formatting elements for use with as.Date() reproduced from statmethods.net.

Symbol

Meaning

Example

%d

day as a number (0-31)

01-31

%a

abbreviated weekday

Mon

%A

unabbreviated weekday

Monday

%m

month (00-12)

00-12

%b

abbreviated month

Jan

%B

unabbreviated month

January

%y

2-digit year

07

%Y

4-digit year

2007

There are many advantages to using the as.Date() format (in addition to proper sorting).

For example, the subtraction between two dates becomes more meaningful and yields the difference in days between them.

As an example, the number of days between Rafael Nadal’s and Andy Murray’s dates of birth can be obtained as

players_dob[1] - players_dob[2]

## Time difference of 353 days

In addition, subsetting becomes also more intuitive and, for example, to find the players born after 1 January 1986 we can simply run:

players[players_dob > "1986-01-01"]

## [1] "Novak Djokovic" "Rafael Nadal" "Daniil Medvedev"

## [4] "Dominic Thiem"

There are many other reasons for using this format (or other date formats).

A more detailed discussion on this topic can, for example, be found in Cole Beck’s notes.

4.1.7 Useful Functions with Vectors

The reason for extracting or creating vectors often lies in the need to collect information from them.

For this purpose, a series of useful functions are available that allow to extract information or arrange the vector elements in a certain way which can be of interest to the user.

Among the most commonly used functions we can find the following ones

length() sum() mean() order() and sort()

whose name is self-explanatory in most cases.

For example we have

length(grand_slam_win)

## [1] 5

sum(grand_slam_win)

## [1] 54

mean(grand_slam_win)

## [1] 10.8

To sort the players by number of grand slam wins, we could use the function order() which returns the position of the elements of a vector sorted in an ascending order,

order(grand_slam_win)

## [1] 4 5 1 2 3

Therefore, we can sort the players in ascending order of wins as follows

players[order(grand_slam_win)]

## [1] "Daniil Medvedev" "Dominic Thiem" "Novak Djokovic"

## [4] "Rafael Nadal" "Roger Federer"

which implies that Roger Federer won most grand slams.

Another related function is sort() which simply sorts the elements of a vector in an ascending manner.

For example,

sort(grand_slam_win)

## Daniil Medvedev Dominic Thiem Novak Djokovic Rafael Nadal

## 0 0 16 18

## Roger Federer

## 20

which is compact version of

grand_slam_win[order(grand_slam_win)]

## Daniil Medvedev Dominic Thiem Novak Djokovic Rafael Nadal

## 0 0 16 18

## Roger Federer

## 20

It is also possible to use the functions sort() and order() with characters and dates.

For example, to sort the players’ names alphabetically (by first name) we can use:

sort(players)

## [1] "Daniil Medvedev" "Dominic Thiem" "Novak Djokovic"

## [4] "Rafael Nadal" "Roger Federer"

Similarly, we can sort players by age (oldest first)

players[order(players_dob)]

## [1] "Roger Federer" "Rafael Nadal" "Novak Djokovic"

## [4] "Dominic Thiem" "Daniil Medvedev"

or in an reversed manner (oldest last):

players[order(players_dob, decreasing = TRUE)]

## [1] "Daniil Medvedev" "Dominic Thiem" "Novak Djokovic"

## [4] "Rafael Nadal" "Roger Federer"

There are of course many other useful functions that allow to deal with vectors which we will not mention in this section but can be found in a variety of references (see e.g. Wickham 2014a).

4.1.8 Creating sequences

When using R for statistical programming and data analysis it is very common to create sequences of numbers.

Here are three common ways used to create such sequences:

from:to: This method is quite intuitive and very compact.

For example:

1:3

## [1] 1 2 3

(x = 3:1)

## [1] 3 2 1

(y = -1:-4)

## [1] -1 -2 -3 -4

(z = 1.3:3)

## [1] 1.3 2.3

seq_len(n): This function provides a simple way to generate a sequence from 1 to an arbitrary number n.

In general, 1:n and seq_len(n) are equivalent with the notable exceptions where n = 0 and n < 0.

The reason for these exceptions will become clear in Section 5.2.3.1.

Let’s see a few examples:

n = 3

1:n

## [1] 1 2 3

seq_len(n)

## [1] 1 2 3

n = 0

1:n

## [1] 1 0

seq_len(n)

## integer(0)

seq(a, b, by/length.out = d): This function can be used to create more "complex" sequences.

It can either be used to create a sequence from a to b by increments of d (using the option by) or of a total length of d (using the option length.out).

A few examples:

(x = seq(1, 2.8, by = 0.4))

## [1] 1.0 1.4 1.8 2.2 2.6

(y = seq(1, 2.8, length.out = 6))

## [1] 1.00 1.36 1.72 2.08 2.44 2.80

This can be combined with the rep() function to create vectors with repeated values or sequences, for example:

rep(c(1,2), times = 3, each = 1)

## [1] 1 2 1 2 1 2

rep(c(1,2), times = 1, each = 3)

## [1] 1 1 1 2 2 2

rep(c(1,2), times = 2, each = 2)

## [1] 1 1 2 2 1 1 2 2

where the option times allows to specify how many times the object needs to be repeated and each regulates how many times each element in the object is repeated.

It is also possible to generate sequences of dates using the function seq().

For example, to generate a sequence of 10 dates between the dates of birth of Andy Murray and Rafael Nadal we can use

seq(from = players_dob[1], to = players_dob[2], length.out = 10)

## [1] "1987-05-22" "1987-04-12" "1987-03-04" "1987-01-24" "1986-12-16"

## [6] "1986-11-06" "1986-09-28" "1986-08-20" "1986-07-12" "1986-06-03"

Similarly, we can create a sequence between the two dates by increments of one week (backwards)

seq(players_dob[1], players_dob[2], by = "-1 week")

## [1] "1987-05-22" "1987-05-15" "1987-05-08" "1987-05-01" "1987-04-24"

## [6] "1987-04-17" "1987-04-10" "1987-04-03" "1987-03-27" "1987-03-20"

## [11] "1987-03-13" "1987-03-06" "1987-02-27" "1987-02-20" "1987-02-13"

## [16] "1987-02-06" "1987-01-30" "1987-01-23" "1987-01-16" "1987-01-09"

## [21] "1987-01-02" "1986-12-26" "1986-12-19" "1986-12-12" "1986-12-05"

## [26] "1986-11-28" "1986-11-21" "1986-11-14" "1986-11-07" "1986-10-31"

## [31] "1986-10-24" "1986-10-17" "1986-10-10" "1986-10-03" "1986-09-26"

## [36] "1986-09-19" "1986-09-12" "1986-09-05" "1986-08-29" "1986-08-22"

## [41] "1986-08-15" "1986-08-08" "1986-08-01" "1986-07-25" "1986-07-18"

## [46] "1986-07-11" "1986-07-04" "1986-06-27" "1986-06-20" "1986-06-13"

## [51] "1986-06-06"

or by increments of one month (forwards)

seq(players_dob[2], players_dob[1], by = "1 month")

## [1] "1986-06-03" "1986-07-03" "1986-08-03" "1986-09-03" "1986-10-03"

## [6] "1986-11-03" "1986-12-03" "1987-01-03" "1987-02-03" "1987-03-03"

## [11] "1987-04-03" "1987-05-03"

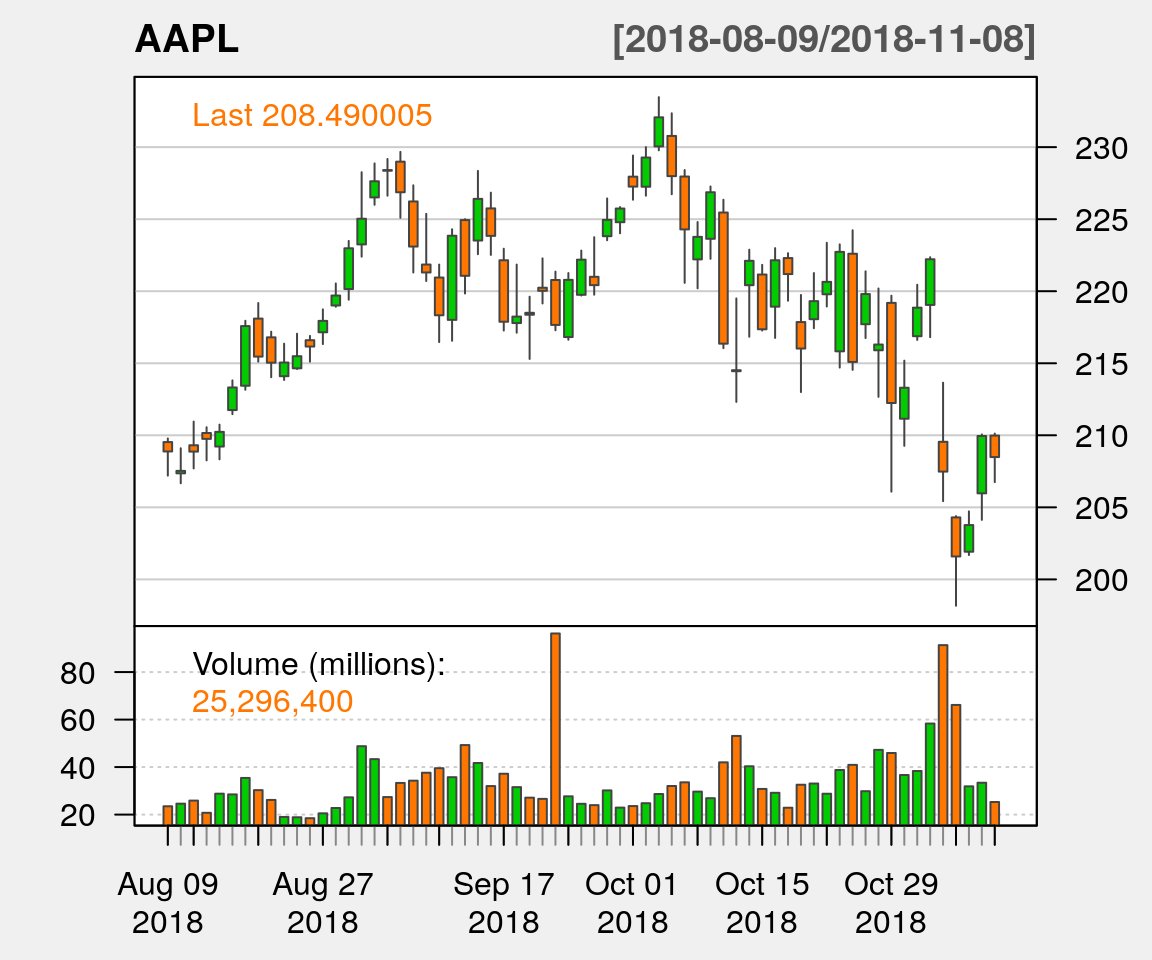

4.1.9 Example: Apple Stock Price

Suppose that someone is interested in analyzing the behavior of Apple’s stock price over the last three months.

The first thing needed to perform such analysis is to recover (automatically) today’s date.

In R, this can be obtained as follows

(today = Sys.Date())